presents

READ THE ARTICLE

For fixed income investors willing to move out on the risk spectrum, emerging market debt is a versatile asset class that still presents a significant yield pick-up opportunity

Emerging market debt should be an integral part of portfolios

Latest insights

Fixed income in a world of falling rates

As shifting politics collides with economic realities, what might this mean for fixed income? Global Head of Fixed Income Jim Cielinski focuses the telescope on prospects for the new year

Stargazing in 2025: Fixed income opportunities

As central bankers shoot for a Goldilocks scenario for their economies, markets seem to believe the porridge is ‘just right’. Head of Secured Credit, Colin Fleury, asks what the risks are and the mixing conundrum for asset allocators

Multi-sector credit: What if 2025 isn’t a Goldilocks year?

Previous insights

Dispelling the myths around European securitised market

JANUS HENDERSON INVESTORS

The modernisation of bond market trading

STATE STREET GLOBAL ADVISORS

Get Britain building again: housing associations key to Labour’s promise

Disrupting the LDI industry

Pics sizes: Small: 620x640 Large: 620x800

Pic size: Large: 424x800 Small: 460x320

Up in quality does not mean ignoring high yield bonds

There is strong appetite for private credit, but the lower liquidity and naturally opaque nature of the asset class can make comparisons with public credit alternatives such as leveraged loans and high yield bonds difficult, says Anand Datar, senior portfolio specialist

Making private credit allocations vs leveraged loans and high yield

There is strong appetite for private credit, but the lower liquidity and naturally opaque nature of the asset class can make comparisons with public credit alternatives such as leveraged loans and high yield bonds difficult

Securitised debt: Opportunity in the European market

Unusual relative value in European CLOs – an opportunity?

Fact vs fiction: Are securitisations ‘opaque’ and ‘risky’?

Analysing the features of European securitised debt dispels the myths that securitisations are ‘opaque’ and ‘risky’. Head of Secured Credit Colin Fleury explores this and evaluates how to assess ESG in securitisations

IMPORTANT INFORMATION These are the views of the author at the time of publication and may differ from the views of other individuals/teams at Janus Henderson Investors. References made to individual securities do not constitute a recommendation to buy, sell or hold any security, investment strategy or market sector, and should not be assumed to be profitable. Janus Henderson Investors, its affiliated advisor, or its employees, may have a position in the securities mentioned. There is no guarantee that past trends will continue, or forecasts will be realised. Past performance does not predict future returns. The information in this article does not qualify as an investment recommendation. Marketing Communication.

Learn more about Janus Henderson Investors

Another concern has been around liquidity, particularly at times of market stress. However, the market has changed dramatically since the GFC. And while the 2022 UK liability-driven investment (LDI) related turmoil resulted in a spike in trading volumes in European securitised, this was absorbed by a range of investors. With the issues driven by rising rates, pension schemes often looked first to sell down floating rate assets, such as securitised, to avoid crystallising larger capital losses in fixed rate bonds. The graph below focuses on trading seen in European CLOs. The subsequent dislocation in securitised prices saw the likes of bank treasuries and private equity firms purchase what remained fundamentally high-quality assets, but at attractive discounts. According to our estimates from market data, over €3 billion of CLOs were sold from September to November 2022 and volumes absorbed well, with over 80% trading to other investors in Europe.[4] Similarly, following the outbreak of Covid-19, a natural widening in bid-offer spreads was matched by increased trading volumes. Within three months of this spread widening, AAA CLO bid-offer spreads were trading at their original levels, compared to European IG bonds taking a year to return to pre-crisis levels.[5]

Illiquid or liquid?

In some respects, securitisations are easier to understand than the complexities of corporate strategy and governance. Our philosophy is in making a complex asset class simple. For example, a collateralised loan obligation (“CLO”) – a portfolio of corporate loans that have been securitised – can be thought of as analogous to a mini bank (as an aggregator of loans), but with several key advantages:

Since the GFC, the securitisation industry has gone through significant structural change. There has been widespread focus placed on the risk management practices of investors, tightening of asset origination criteria, stronger transparency requirements, and tightening of rating agency standards, returning confidence to the market and increased its robustness. Since 2019, the implementation of the European Securitisation Regulation (SECR) has further tightened requirements around the asset class. For example, originators are now required to have “skin in the game”, retaining at least a 5% stake of a securitised assets’ net economic interest to guard against the type of moral hazard seen in the lead-up to the GFC.

Strong demand for CLOs through market volatility while prices quickly normalised

Source: Janus Henderson Investors and Deutsche Bank, March 2023. A measure of publicly reported trading volume in the market, “Bids Wanted in Competition” (or BWIC) are auction processes run by end investors to sell bonds. Past performance does not predict future returns.

“While securitisation does involve a layer of complexity for non-experts, with education it is straightforward...”

Colin Fleury, head of Secured Credit

CONTRIBUTOR

Following the GFC, complex, risky and illiquid are labels that some investors associate with securitised debt. Head of Secured Credit, Colin Fleury, deconstructs these myths surrounding the asset class

Firstly, it is worth noting that even in North America aggregate losses across the securitisation market during the GFC were around 6% – clearly far higher than expectation, but in our view the issue was more where some of the losses were concentrated and the overall scale of the market. Credit enhancement included in securitisations offer support to high-rated debt tranches and provide substantial coverage for extreme levels of collateral losses. For a AAA CLO, for example, the typical credit support is 40% – that is, until cumulative collateral losses exceed 40%, the AAA notes do not take a capital loss. This is five times greater than the worst collateral losses seen in the asset class. In fact, no European AAA, AA and A-rated CLO tranche has ever defaulted.[3]

Risky or resilient?

A lack of transparency and complexity have been arguments used to stigmatise securitised products. The SECR regulation established clear guidelines requiring the production of loan level data in standardised formats, with full disclosure of data required. It also introduced a voluntary “Simple, Transparent, Standardised” label for securitisations,[1] where issuance of these high-quality straightforward structures has grown over the last few years.[2] As a consequence, there has been increased standardisation and transparency in structures. While securitisation does involve an additional layer of complexity for non-experts, we think that with some education, most investors will find the process and structures quite straightforward. Simply put, while corporate bonds provide access to a single loan and single borrower, securitisation gives investors access to a pool of loans and borrowers. Securities are divided into classes – or tranches – and ranked according to their credit quality by a securitisation manager. Investors can then purchase securities in the tranche that suits their risk preference.

Complex or simple?

RETURN TO HOMEPAGE

>

<

OTHER ARTICLES FROM JANUS

Income opportunities: the case for bonds now

Fixed Income opportunities: evaluating spreads vs. yields

3 / 3

Interest rates – opportunities and challenges

Embracing flexibility in strategic bonds

2 / 3

Prepared for landing? 2024 mid-year fixed income outlook

Climate Transition: Avoid? Invest? Engage?

1 / 3

Fixed Income opportunities: Evaluating spreads vs. yields

A reformed sector

• • •

Investors have visibility of every loan that sits in the CLO collateral pool, which is not the case with bank loan books. When banks run into trouble, it’s often due to a lack of access to funding, whereas with securitisations, asset and liability terms are matched. Whilst there’s often ambiguity in the impact of interest rate moves on bank’s assets and liabilities, securitisation structures don’t take material interest rate risks.

While the fallout from the GFC has somewhat tainted the reputation of the sector, the structural developments seen since – facilitated by regulation as well as independent change enacted by the industry – has revived interest in securitised and brought confidence back to the market. Assumptions that securitised is a complex, risky and illiquid asset class can be dismissed under closer examination. We believe investors can benefit from its notable defensive qualities and help diversify portfolios away from traditional fixed income. Though it remains a specialist asset class, investors should take comfort that the common misconceptions surrounding European securitised are just that – misconceptions.

Defensive, resilient and diverse

Sources 1. Criteria on simplicity include requirements on homogeneity of the underlying exposures, underwriting standards and collateral credit quality. Standardisation requirements include early amortisation triggers, performance trigger-based reversion to sequential paydown, and “appropriate” mitigation of interest rate and currency risks. Transparency requirements include provision of a liability cash flow model and at least five years’ historical default and loss data for assets similar to the transaction’s underlying collateral. S&P Global. Meeting such criteria means the assets are eligible for preferential capital treatment. 2. AFME, as at the end of 2023. 3. Moody’s Investors Services, Janus Henderson Investors. Please note defaults and losses are for overall market, CLO transactions due to restrictive eligibility criteria typically experience lower default rates, 2023. 4. Janus Henderson Investors and European CLO dealers. 5. Janus Henderson Investors, based on observed average daily dealer bid/offer spreads from CLO dealers, 2023.

OTHER ARTICLES FROM JANUS HENDERSON

4 / 4

3 / 4

2 / 4

1 / 4

Important information For Professional Clients only and not to be distributed to or relied upon by retail clients. Past performance is not a guide to future performance. Opinions and examples represent our understanding of markets: they are not investment recommendations advice. All data is sourced to Aegon Asset Management UK plc unless otherwise stated. The document is accurate at the time of writing but is subject to change without notice. Data attributed to a third party is proprietary to that third party and is used by Aegon Asset Management under licence. Aegon Asset Management UK plc is authorised and regulated by the Financial Conduct Authority. Adtrax 6105984.1; Expiry 30 April 2025

James Briggs, portfolio manager

Richard Taylor, credit analyst

AUTHORS

Important information For Professional Clients only and not to be distributed to or relied upon by retail clients. Past performance is not a guide to future performance. Opinions and examples represent our understanding of markets: they are not investment recommendations advice. All data is sourced to Aegon Asset Management UK plc unless otherwise stated. The document is accurate at the time of writing but is subject to change without notice. Data attributed to a third party is proprietary to that third party and is used by Aegon Asset Management under licence. Aegon Asset Management UK plc is authorised and regulated by the Financial Conduct Authority. Adtrax 6105984.2; Expiry 30 April 2025

A government that has prioritises housing starts and more generous funding should reduce pressure on housing associations’ business risk profiles, balance sheets and FCF margins. LTV and ICR metrics are set to improve from additional funding and as development sales roll in. Such 'generous’ funding does not necessarily translate into more funds, rather subsidising more of the new build cost. Money earmarked for social housing has actually been returned to government as housing association grant applications have declined due to them covering so little of the total building costs – and therefore risk.

Changing fundamentals

We believe that providing affordable and sustainable housing is a core function of a western government and the outsourcing funding for this creates moral hazard and is arguably not practical. The interest rate environment and progressive cuts in government funding discussed earlier have raised legitimate concerns around the ability of housing associations to meet demands for greater, greener supply. We believe supporting housing associations in their engagement with the government is important. Their role goes beyond providing affordable accommodation to other functions such as helping to reskill unemployed people and debt management.

More than a social factor

Given this reliance on social housing, political infrastructure is a key determinant in meeting housing targets. While the Conservative Government has had much to contend, it is hard to argue that housing was a top priority despite the launch of the Affordable Housing programme in 2016. The UK has had 16 housing ministers since 2013, which has been an obstacle to long-term housing policies and funding. The new Labour government has made housing a priority, targeting 1.5 million new homes over the next five years.

Labour’s promise

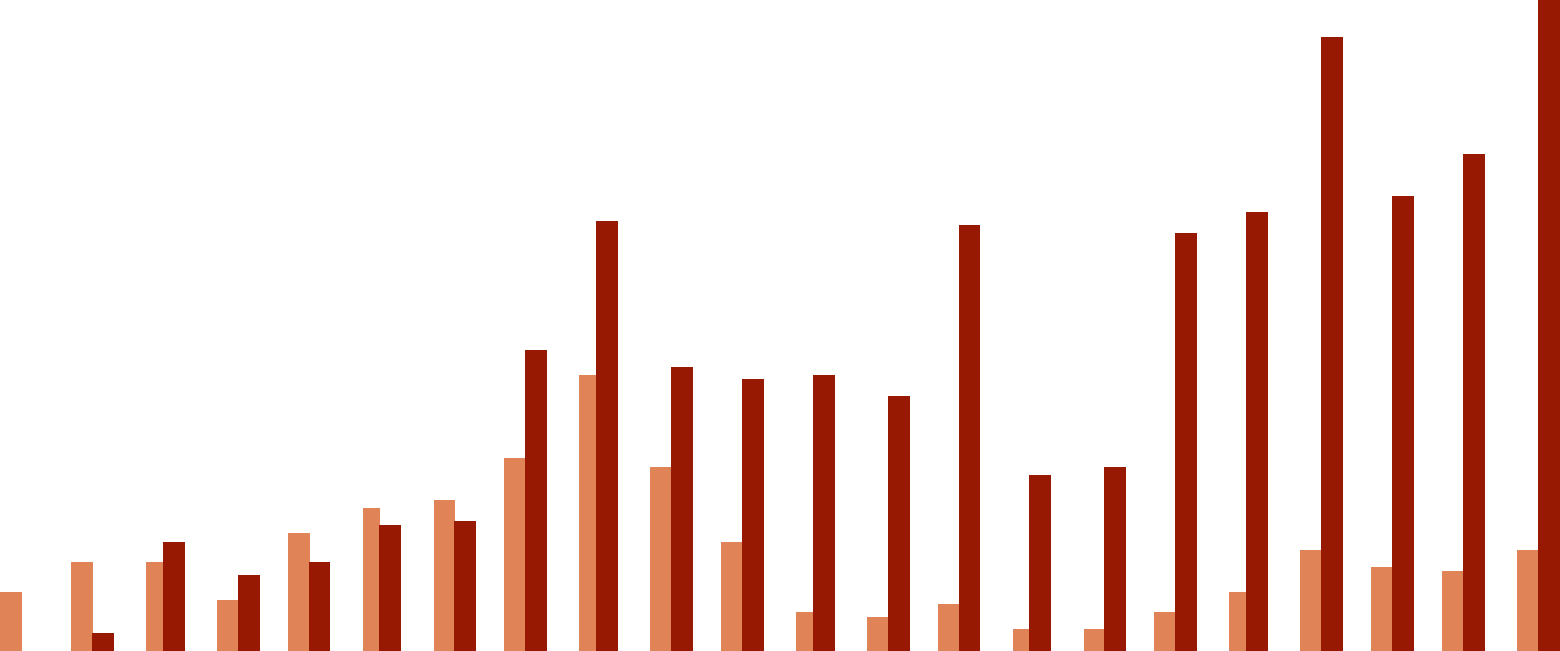

The UK housing market has been undersupplied for decades. A decline in housing starts has been driven almost exclusively by subdued social housing activity – which now makes up 20% of housing starts. The primary delivery mechanism is housing associations, rather than local councils. From the 1950s to 1980s, this was around 50%,[1] although this must be viewed against a different economic climate characterised by lower home ownership (versus renting). Housing associations were public bodies at that time, but they are now privatised. The government is core to the financial and credit profile of housing associations as well as their operational risk. What has changed is the funding supplied by central government (Figure 1).

An undersupplied market

Figure 1: Housing association gross investment expenditure, including private finance, in England

Source: Chartered Institute of Housing, 2024 UK Housing Review, DLUHC local authority level capital expenditure and receipts, Homes England annual report, National Audit Office (2022) Affordable Homes Programme since 2015 and authors’ estimates of private finance, indicative only, 2024.

“Housing associations offer investors the opportunity to benefit from improving credit fundamentals...”

CONTRIBUTORS

Labour’s promise of delivering 1.5m homes necessitates using housing associations. Credit analyst Richard Taylor and portfolio manager James Briggs from Janus Henderson’s Global Credit Team discuss how this has changed the prospects for the sector

So how has punchy housing targets and the absence of sufficient funding impacted housing associations? They have increased balance sheet debt (resulting in higher loan-to-value – LTV – rates and lower interest coverage (ICR ratios), plus public debt issuance. This materially eroded their financial and credit metrics as margins have been squeezed, affecting free cashflow (FCF) and culminating in credit rating downgrades. Additionally, business risk has increased as they cross-subsidise funding social housing starts with proceeds from market-facing activity, such as housing development. There has been an accompanying reduction in SHL (social housing lettings) income, with the sector average on a downward trajectory over 2019 to 2023, according to Janus Henderson estimates. Nevertheless, lower rental income has also depressed housing budgets and the ability to buy sites for development. This pressure has coupled with costs to meet higher building standards from a safety and decarbonisation standpoint. We have seen the cost of fire remediation work result in rating downgrades for housing association credits.

Doing more with less

Housing associations can play a pivotal role in solving the UK housing crisis in our view, offering investors the opportunity to benefit from improving credit fundamentals alongside a positive ESG story. Housing associations typically haven't defaulted in the past as the government has stepped in to encourage the takeover of distressed entities. But as we have seen with local councils, implied support is not an explicit guarantee. With Labour’s new homes target in focus, this could pressure business models and separate stronger companies from the weaker companies. This is why taking an active investment approach, with focused credit research, makes sense. Given the better prospects, we are dialling up our risk within the HA sector in the investment grade space. We are focused on names with high social housing lettings (SHL) exposure, solid ICR, operating surplus and FCF, as dispersion in the sector is set to increase.

Dispersion to increase

“The cost of fire remediation work has resulted in downgrades for housing association costs...”

Source 1. Berenberg, 4 June 2024.

Marketing Communication Important Risk Information ssga.com | State Street Global Advisors Worldwide Entities The information provided does not constitute investment advice and it should not be relied on as such. It should not be considered a solicitation to buy or an offer to sell a security. It does not take into account any investor’s particular investment objectives, strategies, tax status or investment horizon. You should consult your tax and financial advisor. The information contained in this communication is not a research recommendation or ‘investment research’ and is classified as a ‘Marketing Communication’ in accordance with the Markets in Financial Instruments Directive (2014/65/EU) or applicable Swiss regulation. This means that this marketing communication (a) has not been prepared in accordance with legal requirements designed to promote the independence of investment research (b) is not subject to any prohibition on dealing ahead of the dissemination of investment research. This communication is directed at professional clients (this includes eligible counterparties as defined by the Appropriate EU Regulator) who are deemed both knowledgeable and experienced in matters relating to investments. The products and services to which this communication relates are only available to such persons and persons of any other description (including retail clients) should not rely on this communication. Past performance is not a reliable indicator of future performance. Investing involves risk including the risk of loss of principal. Index returns are unmanaged and do not reflect the deduction of any fees or expenses. Index returns reflect all items of income, gain and loss and the reinvestment of dividends and other income as applicable. Diversification does not ensure a profit or guarantee against loss. Bonds generally present less short-term risk and volatility than stocks, but contain interest rate risk (as interest rates rise bond values and yields usually fall); issuer default risk; issuer credit risk; liquidity risk; and inflation risk. These effects are usually pronounced for longer-term securities. Any fixed income security sold or redeemed prior to maturity may be subject to a substantial gain or loss. ETFs trade like stocks, are subject to investment risk, fluctuate in market value and may trade at prices above or below the ETFs net asset value. Brokerage commissions and ETF expenses will reduce returns. International Government bonds and corporate bonds generally have more moderate short-term price fluctuations than stocks, but provide lower potential long-term returns. Investing in high yield fixed income securities, otherwise known as “junk bonds”, is considered speculative and involves greater risk of loss of principal and interest than investing in investment grade fixed income securities. These Lower-quality debt securities involve greater risk of default or price changes due to potential changes in the credit quality of the issuer. Investing in foreign domiciled securities may involve risk of capital loss from unfavourable fluctuation in currency values, withholding taxes, from differences in generally accepted accounting principles or from economic or political instability in other nations. Investments in emerging or developing markets may be more volatile and less liquid than investing in developed markets and may involve exposure to economic structures that are generally less diverse and mature and to political systems which have less stability than those of more developed countries. The views expressed in this material are the views of Srinivasan Margabandu as of April 30, 2024. and are subject to change based on market and other conditions. This document contains certain statements that may be deemed forward-looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected. The trademarks and service marks referenced herein are the property of their respective owners. Third party data providers make no warranties or representations of any kind relating to the accuracy, completeness or timeliness of the data and have no liability for damages of any kind relating to the use of such data. The whole or any part of this work may not be reproduced, copied or transmitted or any of its contents disclosed to third parties without SSGA’s express written consent. All information is from SSGA unless otherwise noted and has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability or completeness of, nor liability for, decisions based on such information and it should not be relied on as such. © 2024 State Street Corporation. All Rights Reserved. 6606656.1.1.GBL.INST Exp. Date: 05/31/2025

Read the full article: Learn about the emergence of different trading styles and the implications for bonds

The market structure for fixed income has been slowly changing from being dealer dominated to an “all-all” model, accompanied by an expansion in electronic trading. Rapid growth in adoption of fixed income ETFs in recent years has provided both a trading instrument and an additional source of liquidity to the entire bond market, with innovative techniques like portfolio trading coming to the fore. Buy-side market participants are diversifying their execution styles, amid the growing use of electronic execution tools for the more liquid and smaller-size tickets being increasingly executed on platforms in an “all-to-all” environment. This better pricing discovery, and market liquidity ultimately impacts returns to investors in the form of lower transaction costs, both explicit (bid-ask spreads) and implicit (opportunity/time cost). Improvements such as predictive adjustments based on market conditions and prior execution results, more accurate real-time pricing, and improvements in data availability are paving the way for more rules-based strategies where implementation reliability and cost are key elements of success.

Figure 1: A steady evolution of incremental changes

12

10

8

6

4

2

0

Global Aggregate

Yield to worst (%)

Global Treasuries

Global Corporates

Global High Yield

EM HC Aggregate

US Aggregate

Euro Aggregate

3.74

1.64

3.16

1.09

4.88

2.61

8.09

6.22

6.76

4.74

4.85

2.42

3.10

0.61

10 year range

Current

10 year median

Source: State Street Global Advisors. The information contained above is for illustrative purposes only. RFQ = Request for Quote. Real-time auction with multiple liquidity providers to select the best price. RFM = Request for Market. Request a two-sided market from a particular provider. Session = Client enters orders to be matched against opposite orders at a specified time and price, concentrating market liquidity to a particular point in time. Streams = Multiple liquidity providers show client continuously updating quotes, in line with market movements, during a clients's request window. PT = Portfollio Trading.

Jim Cielinski, CFA global head of fixed income

The bond market is evolving with increased electronic trading and the growth of fixed-income ETFs, leading to improved liquidity and lower transaction costs that encourage systematic fixed-income investing

Ever since the 1980s, advancements in technology have enabled financial markets to move continuously towards “electronification” – or electronic trading – and the use of technology throughout a trade lifecycle: execution, clearing and settlement. In this paper, as we focus on trade execution, we use “electronification” to refer to the transfer of ownership of a security by matching counterparties through an electronic platform. Electronic trading has facilitated the goals of lowering costs, increasing speed and reliability of execution, enhancing risk management, or generally improving the market structure for trading any over-the-counter (OTC) instrument. However, the benefits that electronic trading begets will vary, particularly economies of scale - which are more readily achieved for markets with standardized products. With primarily exchange-traded products such as equities, the focus of electronification is on speed, whereas for primarily OTC-traded markets such as bonds, the focus is on improving the speed and agility necessary to access liquidity across different counterparties and trading platforms, while employing an increasing array of protocols to do so.

The evolution of fixed income trading

OTHER ARTICLES FROM STATE STREET

Article at a glance:

“Digitization of the trading process has resulted in emergence of a new breed of electronic trading platform...”

Adoption of electronification has not been uniform across the fixed-income product landscape. As shown in Figure 2, variability in market size, liquidity, number of instruments, minimum lot size, types and nature of market participants, as well as available trading protocols have led to varying levels of adoption across the fixed income spectrum. In addition, there exists a spectrum within electronification itself, depending on the nature of the underlying market and segmentation within its securities. Using US Treasuries as an example, 65% trade electronically. Roughly half that volume is via the Request for Quote (RFQ) protocol on the lower end of the spectrum. This mix changes depending on market volatility, issuance patterns, age-distribution (on vs off-the-run), etc. We also see a broader network effect in play in that, once an inflection point is reached, adoption of electronification and concomitant volumes quickly increase – this has been the case with FX spot, US Treasuries, cash equities, and equity options. At the moment, US and European investment grade (IG) and high-yield (HY) corporate bonds are getting close to that inflection point, so we focus more on those markets in this piece. However, it is a truly global phenomena, with the adoption of e-trading starting to take hold in major Asian and Latin American markets as well, particularly in hard currency bonds, which are increasingly being executed on electronic RFQ platforms, as opposed to other less-structured online channels.

Adoption: Electronification, ETFs, and portfolio trading

• • • • •

Voice 1: Few Major Dealer Liquidity Pool Price Takers

Electronic 1: Many Expanded with Smaller, Regional Dealers RFQ, Dealer Inventory

Electronic Open Trading Expanded: with ETF Market Makers Expanded: Inventory, RFM, Session

Electronic, Auto Open Trading All-All Liquidity Pool Expanded: Streams, PT, Rules based Automation

Electronic, Auto Open Trading All-All Liquidity Pool Expanded: Dynamic Workflow Automation

1990

2000s

2010s

2020s

2024+

Figure 2: Electronic trading adoption across markets

Source: Flow Traders, Coalition Greenwich, SSGA Estimates. For Illustrative Purposes Only.

Mostly Voice

Moving Towards Electronic

Post Inflection Point

Highly Electronic

Munis (10-15%) EMD ( 20–25%) Leveraged Loans (<10%) Custom Swaps (<10%)

US IG (35-40%) EUR IG (40–45%) US HY (20–25%) EUR HY (25–30%)

US Treasuries (65-70%) European Govt (75–80%) FX Forwards (50%) Precious Metals (50%) Covered Bonds (40–50%)

Spot FX (90+%) Equity Options (90+%) Cash Equities (90%) UST Futures (90%) CDX Indicies (80–90%)

Historically, bond trading was dominated by dealers interacting with their clients by voice, while inter-dealer brokers acted as intermediaries among dealers themselves. These days, dealers facilitate movement of those bonds, and are able to quickly source the other side of the trade via electronic markets, with little or no holding period in between. Digitization of the trading process itself has resulted in emergence of a new breed of electronic trading platforms, which try to seamlessly connect investors, dealers, and other type of market participants in the quest to find avenues for new sources of liquidity. The buy-side asset management firms have stepped in as well, evolving from a traditionally passive role as a price taker, into a forceful market participant – as a price maker via the new trading venues, while actively shaping trading protocols, as well as providing liquidity in all-to-all platforms for anonymous (no market impact) trading. Figure 1 shows the consistent evolution of the fixed income trading ecosystem.

GO BACK

VIEW MORE

1 / 2

2 / 2

Making private credit allocations vs leveraged loans and high yieldr?

Disclosure Marketing Communication ssga.com | State Street Global Advisors Worldwide Entities For institutional / professional investors use only. Investing involves risk including the risk of loss of principal. The whole or any part of this work may not be reproduced, copied or transmitted or any of its contents disclosed to third parties without SSGA’s express written consent. All information is from SSGA unless otherwise noted and has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability or completeness of, nor liability for, decisions based on such information and it should not be relied on as such. The information provided does not constitute investment advice and it should not be relied on as such. It should not be considered a solicitation to buy or an offer to sell a security. It does not take into account any investor's particular investment objectives, strategies, tax status or investment horizon. You should consult your tax and financial advisor. The information contained in this communication is not a research recommendation or ‘investment research’ and is classified as a ‘Marketing Communication’ in accordance with the Markets in Financial Instruments Directive (2014/65/EU) or applicable Swiss regulation. This means that this marketing communication (a) has not been prepared in accordance with legal requirements designed to promote the independence of investment research (b) is not subject to any prohibition on dealing ahead of the dissemination of investment research. This communication is directed at professional clients (this includes eligible counterparties as defined by the appropriate EU regulator) who are deemed both knowledgeable and experienced in matters relating to investments. The products and services to which this communication relates are only available to such persons and persons of any other description (including retail clients) should not rely on this communication. Bonds generally present less short-term risk and volatility than stocks, but contain interest rate risk (as interest rates raise, bond prices usually fall); issuer default risk; issuer credit risk; liquidity risk; and inflation risk. These effects are usually pronounced for longer-term securities. Any fixed income security sold or redeemed prior to maturity may be subject to a substantial gain or loss. Equity securities may fluctuate in value and can decline significantly in response to the activities of individual companies and general market and economic conditions. © 2024 State Street Corporation – All rights reserved. Tracking Code: 7186722.1.1.EMEA.INST Expiry Date: 03/31/2025

Learn more about Liability Driven Investment

Schemes change their liability-driven investment (LDI) manager for various reasons. Paramount among them is the choice of lower fees. Schemes also seek to benefit from an improved level of service, better-quality and timely reporting, and a deeper level of engagement with their LDI provider. More recently, we have seen an increase in schemes choosing State Street Global Advisors as their LDI manager. Improved portfolio efficiency, better-quality and customized reporting, and lower fees could be some of the ways clients have benefitted from switching to State Street Global Advisors, with minimal disruption or transition costs. State Street Global Advisors’ ambition is to disrupt the existing LDI industry through its innovative and technology-led approach to LDI portfolio management and meet the ever-changing needs of pension schemes in volatile markets.

State Street Global Advisors’ ambition is to disrupt the existing LDI industry through its innovative and technology-led approach to LDI portfolio management and meet the ever-changing needs of pension schemes in volatile markets. Here, the group explains why

As part of the transition, the collateral efficiency of the portfolio can be reviewed and, where appropriate, improved. Many of the clients who we have onboarded have seen such improvements in collateral efficiency help reduce portfolio leverage and deliver material savings in terms of ongoing funding costs. An example is a portfolio that recently transitioned across to our LDI team. Its new design involved switching into more collateral-efficient bonds at each five-year tenor point across the curve, resulting in a reduction of leverage, hence saving the client over 15 basis points on exposure annually in funding costs (at prevailing funding rates, as of 15 March 2024).

Portfolio efficiency

Through our relationship with Van Lanschot Kempen Investment Management, our dedicated transition project management team have been able to transition clients quickly, efficiently and at minimal cost. We have moved clients with pooled and segregated exposures—portfolios that have derivatives and repo positions—for little or no transaction cost and with no out-of-market exposure. In collaboration with the investment consultant, we can model the current exposure of the LDI mandate with the incumbent manager and propose trading or transfer of assets that would replicate the existing level of hedging against the liabilities to create a new LDI portfolio. To this end, we will first determine the suitable transition period depending on the amount of trading needed. Throughout the transition, our LDI team will provide regular updates on the progress. Finally, upon completion, we will provide a report on the transition, with a detailed review of the portfolio before and after trading.

Get the transition right

Why change your LDI manager?

“We can model the current exposure of the LDI manadate with the incumbent manager and propose transfer of assets to replicate the existing level of hedging against the liabilities...”

Common client concerns while changing the LDI manager often focus on the market risks and transaction costs involved. Let us look at some of these considerations:

The usual concerns

A common dealing date can be agreed upon between the incumbent manager and State Street Global Advisors to avoid any out-of-market exposure. If holdings are in unleveraged and leveraged gilts, or index-linked gilt funds, the transition can usually happen without transaction costs. Transition of swap-based funds may incur some transaction costs, but, where of benefit to the mandate, there could be a move from swap to gilt-based funds to alleviate the transaction cost of entering new swaps. This may also make sense from the perspective of relative value, as well as reducing basis risk, if the scheme has gilt-based liabilities. Depending on the size, the transition can be spread across multiple dealing days to minimise transaction costs and market impact.

Pooled Fund Investors

• • • •

State Street Global Advisors can often simply step in on the account managed by the incumbent manager at no cost to the client. We have a dedicated and experienced team of specialists that handle in specie events, ensuring that unleveraged LDI assets can transition at no cost or with out-of-market exposure. Where the portfolio includes derivatives, there are several approaches to help avoid out-of-market exposure and minimise or eliminate costs depending on the type of instrument and legal agreement; for example:

Segregated mandates

Cleared swaps can be ported at the clearing house with no out-of-market exposure Depending on the nature of the legal documentation, it is possible to novate bilateral swaps to a new account, with no out-of-market exposure or transaction costs. Transition of repo portfolios can also be completed with no out-of-market exposure, either through aligning roll dates with the incumbent manager or, where necessary, executing back-to-back trades with a broker (with no transaction cost or change to underlying trade terms).

1. 2. 3.

While there may be one-off costs related to transitioning to a new manager, they could quickly be outweighed by the benefits made available to the scheme. We outline these benefits below:

About State Street Global Advisors and LDI

LDI remains a complex part of client portfolios. We offer a tailored service and speedy analysis that clients may not get with their incumbent managers. With the increased volatility in the rates markets over the last two years, clients have welcomed the timely insights from our portfolio managers to discuss the impact of market moves on their portfolios, but also our ability to facilitate transitions and changes in their mandates.

Improved level of service

We offer daily access to LDI portfolio valuation and analytics reports, including all the information available to our portfolio managers. Along with clients and their advisors, we can build bespoke daily reports in a format that best suits their requirements. These reports are complemented by our comprehensive weekly and monthly reporting, providing clients all the details relevant to their portfolios, including stress test analysis and, importantly, performance and attribution reporting.

Improved reporting

Schemes may benefit from paying lower management fees by considering other LDI providers. The savings here could very quickly dwarf any transition costs. With the One State Street solution, our schemes can benefit from the efficiencies and pricing of operating all services from asset management to custody as one relationship. Clients may also benefit from our scaled global asset management business across cash, fixed income and equity.

Lower fees

We have a technology-led approach to portfolio management. At the heart of this enterprise is the Charles River Investment Management Solution (CRIMS), a system designed to manage every aspect of a LDI mandate, including portfolio management, trading, compliance and collateral management, allowing us to not only manage portfolios accurately and with scale, but to also provide state-of-the-art, timely reporting to clients, including performance attribution.

Technology-led portfolio management

Sources 1. Bloomberg, ICE BofA Global High Yield Index, total returns in US dollars, 30 September 2022 to 30 September 2024. Past performance does not predict future returns. 2. Bloomberg, ICE BofA US High Yield Index, ICE BofA Euro High Yield Index, 30 September 2024. Yields may vary over time and are not guaranteed. 3. Bloomberg, ICE BofA US High Yield Telecommunications Index, total return in US dollar from 30 June 2024 to 30 September 2024. Past performance does not predict future returns.

Read the full article

We said at the beginning that high yield bonds are not universally loved. Investors see attractions from the yield but are wary about tight spread levels. Part of this reflects a preference for rate sensitive assets over credit as well as some de-risking ahead of the US election. In our view, this is good. If favouring high yield over investment grade was popular then the asset class would be more vulnerable to sell-offs. As things stand, high yield is in the bucket that asset allocators view with caution. In the past few weeks we have seen merger and acquisition activity in the telecommunication market, with Verizon bidding for Frontier Communications – a company that essentially reunites Verizon with some of the fibre network assets it sold back in 2017.

The merger and acquisition activity has the potential to create synergies and reduce costs but we think some of this re-rating can be linked to the theme of artificial intelligence and the increased need for data transfer. Fibre networks are being revalued as a useful transmission tool. What this means is that a high yield company such as fibre network business Lumen, which over-expanded and over-levered its balance sheet, in our view now has considerable growth potential because it has the hard assets of a global fibre network in place. Whether it is consolidation or a re-evaluation of assets in a business, we are seeing market sentiment towards telco assets, particularly those with fibre businesses, turn more favourable and that has caused spreads to come down and bond prices to rise as yields have fallen sharply in the sector. Over the course of the third quarter of 2024 alone, the telecoms sector of the US high yield market returned 11%. [3] Yet yields and spreads remain elevated, which could offer the prospect for further gains.

Positive re-rating

Taken together, we think the cautious attitude towards high yield may be misplaced and (putting geopolitics aside) the positive run in high yield can continue so long as the US economy holds up. That does not mean being complacent. We need to be mindful that idiosyncratic risk is ever present and high yield bonds are rated lower quality for a reason. Challenges exist. These challenges can and are being dealt with, which explains the relatively low default rates experienced during the most recent tightening cycle. The tightness in spreads means little room for disappointment so earnings results alongside economic data will command particular importance. For now, economic data continues to point to a soft landing and central bank rate cuts should help to bring down bond yields. High yield bonds typically have shorter maturities than investment grade bonds on average, so a decline in the front end of the yield curve has the potential to help boost total returns and cut refinancing costs. So far, rate cuts have been in response to falling inflation and as a precautionary measure to ward off economic softness. Provided that remains the case, we think high yield continues to offer attractions within a diversified portfolio.

Due diligence

Part of that strong return has come from capital gain, but nearly 60% came from income. Time and again, throughout history, it is income that typically drives the long-term returns on assets. Today, US high yield is yielding approximately 7.0% and European high yield 5.8%. [2] These are not the most generous yields, but they are not mean either and certainly not in the context of current inflation levels. A cursory glance at the yield on US high yield versus US inflation (headline Consumer Price Index) suggests that current yield levels are about standard for the last 20 years outside the spikes that occur in crises.

High yields offer a head start

It is at the credit spread level that valuations on high yield bonds look rich but just because they are at the tighter (or low) end of their range does not mean they cannot go tighter. A soft landing is the type of environment that could allow credit spreads to tighten further, since moderate economic growth should allow cashflows to be maintained and reduces the risk that central banks would revert to raising interest rates again. Currently, tight spreads are the market’s way of signalling that investors are reasonably comfortable to accept credit risk (the risk that a corporate borrower is unable to meet their debt repayments). This is evident in bond issuance where the supply of corporate bonds has been met by plenty of demand from investors. Companies can access markets, and this is helping to keep the default rate relatively low considering we have just come through a tightening cycle.

Spreads tight but could they go tighter?

A common refrain amongst the investment community is that with central banks moving to cut rates, inflation must be tamed and economic strength is the new concern. In such an environment, it makes sense to move up in quality within corporate bonds because you will be more exposed to bonds that are more interest rate sensitive and less exposed to credit sensitive assets. We do not disagree with the central premise of this argument. Where we think it falls down is when it is applied simplistically. One could quite easily have assembled a convincing case for an impending recession in the past 24 months – inverted yield curves, weak purchasing manager indices, subdued consumer confidence – and avoided high yield bonds in their entirety. To do so would have been costly as global high yield bonds, represented by the ICE Global High Yield Bond Index, delivered a total return in US dollars of 31.9% over the 24 months to 30 September 2024. [1]

“Investors see attractions from the yield but are wary about tight spread levels. Part of this reflects a preference for rate sensitive assets over credit as well as some de-risking ahead of the US election”

Yield on US high yield bonds versus US inflation

Source: LSEG Datastream, ICE BofA US High Yield Index, yield to worst, Bureau of Labor Statistics, US Consumer Price Index (CPI) inflation rate, year-on year percentage change, seasonally adjusted, 30 September 2004 to 30 September 2024. Yield to worst is the lowest yield a bond (index) can achieve provided the issuer(s) does not default; it takes into account special features such as call options (that give issuers the right to call back, or redeem, a bond at a specified date). Yields may vary over time and are not guaranteed.

Yield

CPI inflation rate

Brent Olson, portfolio manager

Tom Ross, CFA, head of high yield / portfolio manager

High yield bonds still have the potential to surprise positively as reflected in the recent re-rating of the telecoms sector, say portfolio managers Brent Olson and Tom Ross

Read the full report

Key features

Why consider European securitised

Offering robust structural controls and credit support, diversification from traditional fixed income and a positive return outlook, we believe there is an excellent strategic case for holding European securitised in a multi-asset portfolio. Investors are able to allocate to diverse structures and underlying asset types, tailoring the risk and return profile of their securitised allocations. The floating rate nature of the sector can also help in managing interest rate risk. Including securitised investments in a multi-asset portfolio has been shown to enahnce returns and reduce risks. This is something we have implemented in a range of client portfolios for many years at Janus Henderson Investors should be mindful securitised is a specialist asset class, where expertise is required for the careful evaluation of the risk and reward profile of each transaction – ultimately those who do undertake the required due diligence should see European securitised play a beneficial role in portfolios.

Accessing attractive yield, diversification and resilience

The European securitised market offers the opportunity to capture risk-reward profiles that are distinct from what can be found among corporate bonds. As well real economy exposures, high quality, floating rate coupons and higher credit spreads than in traditional corporate credit all contribute to this. The different sub-sectors have various features, which we explain here, and how the sector offers access to attractive yields, diversification and resilience.

While the European securitised market comprises a range of structures with a diverse pool of assets, there are some common features: Real economy exposures: Given the nature of the underlying collateral, the European securitisation sector offers access to different consumer-driven and ‘real economy’ risks, diversifying from corporate credit. High quality: The pooling of risk of the underlying loans and credit enhancement features results in an overwhelmingly high-quality market, reflected in a high proportion of the structures rated AAA. Such structural protections, high asset quality as well as natural deleveraging from amortisation has enabled the European securitised sector to exhibit a very low default rate through economic cycles and periods of broad macro stress.

Attractive risk and return profiles: Securitised generally has a higher average credit quality than corporate bond indices and a shorter spread duration (see table below). Amortising structures and the short-dated nature of large parts of European securitised naturally lowers spread duration. Similarly, the floating rate nature of the asset class limits the impact of moves in interest rates (which amplifies the volatility of mark-to-market returns in longer duration fixed income). Resultingly, risk-adjusted returns stack up well relative to other areas of fixed income. Improved diversification: The sector’s diversification potential is reflected in the low correlation of the European securitised sector to other credit fixed income asset classes. One of the most comparable is high quality IG credit, relative to which European securitised assets tend to show lower volatility. Aside from heighted correlation during periods of extreme market stress, European securitised assets tend to trade with low beta to IG credit, which results in less volatility in excess returns. Managing portfolio duration: With the vast majority of the European securitised market being floating rate, investors can access credit excess returns whilst separately managing their interest rates hedging strategy, or hold duration elsewhere in their fixed income allocation when they deem it attractive to do so.

Source: Janus Henderson Investors, Bloomberg, as at 31 August 2024. ICE BofA Euro Corporate Index shown.Note: Data shown is referencing Janus Henderson Asset Backed Securities Fund. 1.Credit spreads are versus SONIA for the ABS Fund. Bond index credit spreads are Swap OAS. 2.Yield shown is yield to maturity hedged to GBP. Euro IG corporate bond yield to maturity hedged to GBP based on the sum of the GBP OIS swap rate that corresponds to the average life of the index and the credit spread. 3.Spread duration is based on modelled base expected average life for the invested portfolio and weighted average lives for securitised asset classes are estimated based on typical weighted average life for the sector. 4.Excludes cash balance. Yields may vary and are not guaranteed. Past performance does not predict future returns.

Characteristics of European securitised sub-asset classes versus credit

Source: Janus Henderson Investors. CRE= commercial real estate.

European securitised at a glance

“Offering robust structural controls and credit support, diversification from traditional fixed income and a positive return outlook, there is an excellent strategic case for holding European securitised in a multi-asset portfolio”

Ian Bettney, portfolio manager

Colin Fleury, head of secured credit

Kareena Moledina, client portfolio manager, lead, EMEA

Denis Struc, portfolio manager

Allocating to the European securitised market opens up access to diverse structures and underlying asset types, allowing investors to tailor risk and return profiles. Here the European Securitised team take a deep dive into the workings of the sector and evaluate the opportunities

Sources 1. Morgan Stanley, 5 November 2024. 2. Around three years. 3. JP Morgan, Janus Henderson, based on observed transactions, 31 October 2024. 4. Janus Henderson based on observed supply, 31 October 2024. 5. The term premium is the additional credit spread, or compensation, received for buying longer bonds overshorter dated bonds. 6. The bid is the highest price an investor is willing to pay for a security. The offer is the lowest the seller (or issuer) is willing to sell the security for. 7. Spread duration is the sensitivity of a bond’s price to a move in its own credit spread. A “higher” spread duration means that the price of a bond is more sensitive to a move in credit spreads.

To put some numbers to this, a AAA CLO spread of 85bps is screening exceptionally tight at around the 10th percentile relative to its range over the last 10 years, whereas 130bps [4] for newly issued securities is just above the median average. All of this begs the question as to what is driving this yawning term premium: in short, the elevated supply of new issue CLOs has been generally issued with longer tenors, keeping those longer-dated spreads wider. Meanwhile, more risk averse investors have been happy to continue to pick up shorter-dated bonds, confident they will receive both their sliver of spread and principal back in the near term. Given the relatively benign environment, with low corporate defaults, we think the long end of the CLO credit curve constitutes good value and could warrant taking on the additional spread duration [7] for what are very high-quality bonds. Looking down the capital stack, new issue AA CLOs are also pricing around historic 10-year median spread levels, at 200bps in the primary market. Simultaneously, short-dated A CLOs, a grade lower, are trading at similar levels in the secondary market. This is shown in Figure 2, which shows where spreads currently sit, relative to the past 10 years, with AA CLOs clearly trading cheaper.

Supply dynamics distort spreads

A steep credit curve emerges

From a relative value perspective then, A rated CLOs look very expensive compared to AAs. Indeed, the ability to buy AA rated bonds in the primary market near the same spread levels and cash price as A bonds in the secondary market (albeit for shorter profiles), we believe highlights some distortion in market pricing. Anecdotally, we are hearing there is significant demand from select North American investors for European A CLOs, which has driven its spreads materially tighter and compressed the spread basis between those two tranches. While neither rotating into new issue AAA CLOs nor exchanging secondary A-rated bonds for AA in primary markets offer a ‘free lunch’, we think both fundamentals and the supply/demand dynamics remain supportive. Investors who can stomach the added spread duration risk could be well compensated.

Assessing relative value

2024 has been a scorching year for European CLO issuance, with around EUR41 billion of gross new supply issued so far [1] and it looks likely to be a post-GFC calendar year record for new CLO creation. Balanced with strong investor demand, this has seen CLO spreads move sideways in recent months, largely on this dynamic. However, a deeper dive into the valuations shows some pricing dislocations. At first glance, spreads for the AAA-rated senior tranches appear tight at current levels, with secondary market spreads for mid-tenor [2] AAA-rated CLO at around 100bps [3] and certain short-dated securities trading inside of 80bps. By contrast, longer-dated new issue AAA CLO is typically pricing nearer to 130bps for top-tier CLO managers [4]. This steep term premium [5] is a relatively uncommon phenomenon, with the CLO credit curve generally quite flat in benign market conditions. As shown in Figure 1, a sample of recent AAA CLO bids and offers [6] evidence a pronounced upward slope to the curve – ie. long-term bonds are pricing with (unusually) wide spreads relative to short-term bonds.

“Given the relatively benign environment, with low corporate defaults, we think the long end of the CLO credit curve constitutes good value and could warrant taking on the additional spread duration”

Figure 2: AA and A CLO credit spread ranges – percentile rank vs history

Source: JP Morgan, Janus Henderson calculations, 31 October 2024. Based on a 10-year lookback of European AA and A-rated CLO spread levels.

Figure 1: European AAA CLO bid-offer spreads show steep curve

Source: Bloomberg, Janus Henderson, 21 October 2024. Based on a sample of live bids and offers on this date for European AAA-rated CLOs. Curves are logarithmic based on this sample. Discount margin (DM) is the average expected return of a floating-rate security (typically a bond) that’s earned in addition to the index underlying, or reference rate of, the security.

Portfolio managers Denis Struc and Ian Bettney explore the supply and demand factors creating distortion in the pricing of European collateralised loan obligations (CLOs), setting out two relative value opportunities that have emerged

Expensive

Cheap

AA CLO

0%

25%

50%

75%

100%

A CLO

Median average

Key features of European securitised debt

Another misconception around the securitised sector is that the ‘opaque’ structures make ESG analysis impossible. The nature and structure of the European securitised market does mean analysis across multiple layers of a transaction, while it is challenging to gather standardised ESG metrics. This requires a specialist approach to ESG analysis. To address this challenge, we are working to promote standardised disclosures from issuers, and to improve the quality and depth of disclosures from across the industry. Given these challenges, it is therefore important to develop proprietary frameworks that enable us to gauge the ESG profiles of these investments using loan and collateral data for the assets financed by our securitised investments. As we develop our frameworks to measure carbon in securitisation markets, we continue to engage collaboratively with international agencies such as the Partnership for Carbon Accounting Financials (PCAF) and European Leveraged Finance Association (ELFA), as well individual issuers across residential mortgage-backed securities (RMBS), auto asset-backed securities (ABS) and collateralised loan obligations (CLOs) to obtain additional data to enhance the accuracy of our carbon estimates. When deciding on where and with who to engage, it is important to identify where we, as investors, have most direct influence.

Clearly defining sustainability objectives is key to a successful engagement programme, which should be well-established and systematic to achieve outcomes. One example of thematic engagement is efforts to improving carbon disclosure from Auto ABS issuers, requesting that they directly provide vehicle emissions data and estimated mileage as part of their loan level data. Three Australian auto issuers have confirmed that they will start providing such loan level emissions data, acknowledging that change is a result of our ongoing engagement with them. It is clear then that a specialist approach to assessing ESG in securitised investments and engagement to facilitate change can help tackle some of the challenges surrounding this endeavour, such as data availability. The defining features that separate the securitised asset classes from investment grade corporate credit warrant consideration from multi-asset investors seeking diversification in portfolios. In the next instalment in our series, we take a deeper dive into the sub-asset classes, looking behind the acronyms in the sector.

Addressing ESG

Securitised debt has been labelled by some investors as ‘opaque’ and ‘risky’. We separate fact from fiction by considering the distinct characteristics that define the asset class and evaluate the risk-reward profile of the securitised sub-sectors against European investment grade corporate credit. We also explore how to assess ESG in securitised investments, tackling data challenges and value chain traceability as well as using engagement to encourage change.

Collectively, these features result in a risk-reward profile that is distinct from what can be found among corporate bonds. Securitised asset classes typically offer higher credit spreads while taking lower spread duration risk and exhibit better credit quality (Figure 2).

While the European securitised market comprises a range of structures with a diverse pool of assets, there are some common features:

Real economy exposures: Given the nature of the underlying collateral, the European securitisation sector offers access to different consumer-driven and ‘real economy’ risks, diversifying from corporate credit. Examples include auto loans, credit card receivables and personal loans. High quality: The pooling of risk of the underlying loans and credit enhancement features results in an overwhelmingly high-quality market, reflected in a high proportion of the structures rated AAA (Figure 1). This compares to the European investment grade corporate bond market having a weighted average credit rating of A-[1]. Such structural protections, high asset quality as well as natural deleveraging from amortisation has enabled the European securitised sector to exhibit a very low default rate through economic cycles and periods of broad macro stress.

• •

Floating rate coupons: Coupons typically reset monthly or quarterly, moving in line with market interest rates (with a spread over prevailing cash rates). Thus, interest rate risk is somewhat negligible. Higher credit spreads: Supply and demand mechanics can result in higher credit spreads than in traditional corporate credit. Less favourable regulatory treatment of the underlying assets on bank balance sheets encourage securitisation to offload such assets. Similarly, banks use securitisation as a funding tool, freeing up capital for other lending activity. Both these factors are supportive for supply.

Sources 1. Janus Henderson Investors, Bloomberg, as at 31 August 2024. ICE BofA Euro Corporate Index.

Securitised and investment grade corporate bond spread versus spread duration profiles

Source: Janus Henderson Investors, Bloomberg, Citi Velocity, Morgan Stanley, JP Morgan, as at 31 August 2024. Weighted average lives for securitised asset classes are used to estimate their spread duration. A Euro Corps = ICE BofA Single-A Euro Corporate Index, AA Euro Corps = ICE AA BofA Euro Corporate Index, BBB Euro Corps = ICE BBB BofA Euro Corporate Index. NC = non-conforming. Yields and spreads may vary and are not guaranteed.

Figure 2: A distinct risk-reward profile versus corporate bonds

Source: Janus Henderson Investors, AFME, European securitised debt outstanding as at 31 March 2024. Based on Moody’s rated securities. For illustrative purposes only.

AAA, 58.2%

Sub-investment grade, 3.4%

BBB, 3.4%

AA-A, 35.0%

Figure 1: European securitised – a high-quality asset class

“Clearly defining sustainability objectives is key to a successful engagement programme, which should be well-established and systematic to achieve outcomes”

AAA Aussie Consumer ABS

AAA Prime UK RMBS

AAA NC UK RMBS

ANC UK RMBS

AA CLOs

A CLOs

BBB CLOs

AAA CLOs

BBB Euro Corp

A Euro Corp

AA Euro Corp

AAA European Consumer ABS

AAA Auto ABS

Private credit strategies have proliferated from direct lending to distressed, mezzanine, venture, opportunistic and has also become more specialized by sector. Direct lending (which is still the largest and most conservative sub-segment) focuses on private asset managers making corporate loans typically to middle market companies (with annual revenues of between US$50 million to US$1 billion). Against a backdrop of public market yields hovering near historical lows until early 2022, private credit (direct lending) delivered attractive excess returns versus leveraged loans and high yield bonds over the three and five year periods to September 2023, compared to the historical average. These excess returns were noticeably higher relative to high yield bonds which faced significant headwinds due to rising benchmark yields and the impact of duration. However, the aforementioned decline in the yield premium commanded by private credit has contributed to a narrowing of the performance gap between the three categories over the past year. We note that the future return prospects for all three categories have improved due to the increase in benchmark rates.

From a portfolio perspective, high yield is the most liquid of the three categories, followed by leveraged loans, both of which are priced on a daily basis. Private credit is typically valued on a quarterly basis, with slower valuation adjustments compared to publicly traded high yield and leveraged loans. These valuation frequency differences can lead to high yield and leveraged loans exhibiting relatively higher volatility levels as measured by standard deviations of quarterly returns. From a portfolio liquidity perspective, we believe the three categories can complement each other and can be used to optimize investor allocations. Since the timing of private credit capital calls are uncertain (and some capital calls can take multiple quarters or years), investors can utilize the better liquidity profile and easier access of high yield bonds or leveraged loans to gain interim sub-investment grade exposure for the committed but as-yet-uncalled capital while being mindful of tactical risks in the segment.

Returns in focus

Since large yield premiums in private credit no longer remain the dominant factor in allocations, investors have to balance the better liquidity, efficiency, and flexibility (suitability for tactical allocations) offered by leveraged loans and high yield versus the customized exposures and strategic nature of private credit to make sub-investment grade allocation decisions. While the yield premium offered by private credit helps enhance portfolio returns, these have shrunk significantly in recent years and the asset category lacks the liquidity and flexibility to opportunistically deploy capital from a tactical asset allocation viewpoint, especially during phases of high market dislocations. The dispersion among the performance of private credit managers is very wide, highlighting how important manager selection and due diligence is to generating expected returns.

Furthermore, the proliferation of private credit strategies and specializations means investors need to fine-tune their portfolio exposures when making strategic asset allocation decisions. In contrast, high yield bonds and leveraged loans present investors with the liquidity and flexibility needed to make tactical asset allocation changes, and can be used effectively and quickly to adjust overall exposure to sub-investment grade credit sectors. This is especially important during periods of significant market dislocations. The higher interest rates today and normalized risk premiums suggest improving total return prospects for both of these categories mean they warrant consideration for strategic asset allocations alongside private credit. An indexed approach to high yield bonds and leveraged loans can also be used to gain broad exposures to these sub-investment grade categories and efficiently harness reliable risk and return outcomes of these credit sectors.

The bottom line

Private credit typically forms part of the alternative investments allocation in investor portfolios, while high yield bonds and leveraged loans fall within general fixed income allocations. However, the high correlations between the total return performance of the three categories serve to highlight the similarities that exist in the underlying credit exposures, including credit sensitivity and cyclicality. Private credit has typically focused on small and mid-sized borrowers, while syndicated loans and high yield borrowers also tend to fall at the lower end of the credit spectrum. In private credit, the average size of the borrower has been growing, although lending to investment grade companies is still at a relatively early stage.

“The proliferation of private credit strategies and specializations means investors need to fine-tune their portfolio exposures when making strategic asset allocation decisions”

“The future return prospects for all three categories have improved due to the increase in benchmark rates”

Source: Bank of International Settlements (BIS), Preqin, SIFMA, International Monetary Fund. * As of June 2023.

Private Credit Assets Under Management

Leveraged Loan Outstanding — USA

High Yield Bonds Outstanding — USA

Private Credit AUM as %of Public Credit (R.H.S)

Click here to read the full report

Our philosophy

Source: State Street Global Advisors as of March 31, 2024.

Within Tight Risk Limits

As an index manager who doesn’t take fundamental bets, we believe we can add value to investors by focusing on two key areas — reducing the cost of implementation and exploiting market inefficiencies within tight risk constraints. To that end we have developed our Investment Approach which is underpinned by a stratified sampling methodology that constantly aims to strike the right balance between minimizing the tracking error and minimizing the cost of implementation.

Where we add value

Emerging economies present superior growth prospects relative to developed counterparts and many have comparatively lower debt burdens. Broad EMD yields are high in absolute terms and an increasing number of EM central banks have embarked on a rate-cutting path, underpinning a growing, albeit guarded, case for consideration of the asset class in investors’ portfolios.

State Street Global Advisors has been running indexed EMD strategies for almost two decades and our experience and expertise has underpinned the growth of this franchise. Our EMD assets under management has continued to grow despite bouts of considerable outflows from the asset class at times.

Trends driving growth in EMD index investing have also been beneficial, including structural improvements in emerging markets. The inconsistent performance of active managers in this space and mixed track record in providing good downside protection during volatile periods has also been a key factor. However, the growth we’ve experienced in our AUM has also been fueled by clients choosing to switch allocations from other index managers.

The success of our approach has seen EMD assets under management at State Street climb from about $5 billion at the end of 2015 to $40.5 billion at the end of March 2024. We have a large and longstanding EM portfolio management team, which is supported by dedicated EM debt traders and portfolio strategists. We partner with clients to help them achieve their investment objectives. We can manage index strategies against both standard and bespoke benchmarks. We have delivered a consistent performance that has very closely tracked, and sometimes outperformed, the relevant EMD benchmark index.

“Trends driving growth in EMD index investing have also been beneficial, including structural improvements in emerging markets”

“Emerging economies present superior growth prospects relative to developed counterparts and many have comparatively lower debt burdens”

2. Exploiting Market Inefficiencies

Harvesting Primary Market Premium

Security Selection

Proactive Management of Index Events

1. Efficient Implementation

Selective Turnover

Minimising Transaction Costs

Minimising Tax Drag (EMD LC)

Sources 1. Carry: A typical definition is the benefit or cost of holding an asset. For a bond investor this includes the interest paid on the bond and potential gains or losses from currency changes.

Despite this macro and political uncertainty, we enter 2025 with both corporates and consumers in decent shape and a banking sector that feels generally sound. The rapid growth of private credit funds in recent years has also reduced reliance on banks for corporate capital needs. When analysing the performance of securitised collateral pools, we have seen some weaker consumer cohorts show increasing delinquency, but generally not far beyond more normal pre-COVID levels. Overall, this cycle does not appear to have seen overly aggressive lending to either consumers or corporates. So while the economic cycle is uncertain, we are not overly concerned that 2025 could bring a material spike to corporate or consumer defaults.

Consumers and corporates stay resilient

Generally, credit spreads in fixed income markets are tight versus long term history and are largely fully pricing in a relatively benign economic landing. However, we see a couple of relative bright spots in loans and securitised debt. Credit spreads in these asset classes are generally more mid-range versus their long-term history, offering both somewhat better carry [1] and a more positive distribution of potential market moves. They are also typically floating (variable) interest rate or relatively short duration, which currently provides extra income, while cash rates remain elevated. If rates decline as forecasted in Figure 1, this would broadly bring them in line with current longer-term interest rates (in other words it is ‘priced in’). There is also clearly the ‘too hot’ scenario where cash rates remain higher than expected and floating rate characteristics prove even more valuable.

Searching for value

For central bankers, navigating their economies to a Goldilocks scenario – where an economy is neither too hot or cold, with moderate growth and low inflation – is the coveted destination. ‘Too hot’ employment, inflation and growth could scupper this. On the flip side, cooling an economy too much could cause growth to undershoot target. The pace and magnitude of easing interest rates is their key tool. Given the different political and macro conditions globally, central bank monetary policy is set to diverge in 2025 to target the ‘just right’ economic conditions. Turning to the UK, Europe and the US, markets expect the European Central Bank to cut most aggressively, followed by the US Federal Reserve and the Bank of England (BoE). This reflects Europe’s ‘too cold’ scenario in terms of sluggish growth, while the US is flirting with ‘too hot’, particularly if the Trump presidency results in a growth or inflation boost. The UK growth outlook does not appear to be markedly better than continental Europe, but government policy and spending may complicate the picture for the BoE. While the expected path for short-term interest rates has remained downward across economies, recent rates volatility has been high, and the extent and pace of cuts has diverged. Changed political landscapes in the US, UK and now potentially Germany and France, add to the uncertainty in the quest for Goldilocks.

As asset allocators, we are facing our own kitchen conundrum in getting the porridge ‘just right’ in our portfolio asset mix to navigate 2025. There is the risk of ‘too hot’ rates volatility, such as a ‘higher for longer’ rate narrative materialising, which could come with a better growth outlook (or may just be the result of unexpected inflationary pressures). This may be an environment that favours high credit quality and short duration securitised or variable rate corporate loans. There is also the ‘too cold’ risk of weaker macro conditions and lower interest rates than currently expected, where even though coupon income may decline with market interest rates, the defensive properties of investment grade securitised debt could prove valuable. It is also important to consider when building diverse portfolios that even though market expectations are for cash rates to decline, they are forecast to remain relatively high, particularly in the US and UK. When combined with the credit spreads on offer from a diverse fixed income portfolio where securities are selected based on credit fundamentals, the overall prospective yield remains attractive.

“There is the risk of ‘too hot’ rates volatility, such as a ‘higher for longer’ rate narrative materialising, which could come with a better growth outlook”

“We enter 2025 with both corporates and consumers in decent shape and a banking sector that feels generally sound”

Figure 1: Cash rates expected to stay relatively high

Source: Janus Henderson, Bloomberg, ICE, as at 26 November 2024. Forward rates based on GBP, USD and EUR OIS curves as at 26 November 2024. Notes: 1M Libor up to 31 December 2020 then SONIA, ESTR, SOFR 1M rates. There is no guarantee that past trends will continue, or forecasts will be realised.

Colin Fleury, Head of Secured Credit

The economy and inflation