Scroll to explore

As the credit market continues to evolve, successful investors will need to be nimble to navigate bond sectors

A year of opportunity amid uncertainty?

Portfolios must be strategically positioned to benefit from lower interest rates, while also safeguarding against potential economic and credit risks. A key challenge will be effectively managing the increased dispersion within the bond market

Two things differentiate Columbia Threadneedle from our investment grade competitors: a bottom-up approach to constructing portfolios, and a real focus on downside risk management

Look to the future now, it’s only just begun

Read our weekly snapshot

16 December 2025

A balancing act

Latest insights

Alpha, an active approach and fundamental research – how we invest in credit

Read more

In Credit

Read snapshot

Over the next 10 years the US dollar will likely surrender another 10% share of global foreign exchange reserves – but there will be no single beneficiary, with 10 different currencies all growing their allocations

FX reserves and the 10-10-10 proposition

Geopolitics will dominate the investment landscape, with increased tariff and sanction regimes affecting trade. As a result of this, market volatility will argue for nimble active portfolio management as the best way to navigate potential headwinds

Economic nationalism will present a constant challenge for investors

Patience will be crucial in 2025. To navigate uncertain market shifts, our focus is on risk-managed yield capture

The fixed income market comes out swinging

As inflation cooled, central banks transitioned from rate rises to a rate cutting cycle, monetary policies loosened and growth gradually slowed. Where do we see things going from here?

EMEA Investment grade examined

There has been speculation that a desire to avoid using the US dollar might encourage the BRICS nations to adopt a gold-backed currency. But there are several questions to ask about such a proposal

Shared BRICS money: basket currency or basket case?

What could be the impact of first-mover and reciprocal tariffs on the USD and Treasury yields?

Watch the US dollar and Treasury yields to understand the potential effects of tariffs

The market reaction to European military defence plans has been enormous, with more volatility expected in bond yields, curves, cross-market spreads and currencies

Germany cuts the debt brakes with defence spending set to soar

The path is uncertain, but a potential ceasefire could bring some respite to the region and could also have significant geopolitical and economic implications

Positioning for a potential Russia-Ukraine war ceasefire

A nimble strategy will be crucial for investors bracing for a fluid economic landscape marked by growth headwinds, policy shifts, and intense scrutiny of the Federal Reserve's next steps

High-quality bonds are an important portfolio diversifier in uncertain markets

With over half of the delinquent loans from the global financial crisis still sit on the books, the conditions are not right for China's stimulus hat-trick

China: Don’t count on a big stimulus package this time

For pension scheme trustees, an integrated solution for LDI and investment-grade credit offers benefits, particularly from an investment and governance standpoint

LDI differentiator: the benefits of an integrated solution with credit

How will policy uncertainty and macro headwinds shape opportunities in fixed income?

Midyear fixed-income outlook: Strategic scenarios for bond investors

To successfully pick winners in the pharmaceutical industry, the most effective approach continues to be a sharp focus on businesses with superior product portfolios and promising development opportunities, a strategy that could transcend the political backdrop.

A bitter pill: what tariffs could mean for pharmaceutical firms and the wider healthcare industry

The AI infrastructure boom is more than a tech story – it’s a fixed income story. Discover how this capital-intensive transformation is creating new opportunities and risks for bond investors.

Bond investors join the AI infrastructure boom

Environmental change isn’t just a humanitarian concern, it’s a mechanical one. From jet engines to toll roads, shifting climates are reshaping military readiness, infrastructure resilience, and the investment case for the companies that build and maintain such assets.

Battling the elements: will climate change reshape defence spending?

Assumptions that underpin the US dollar’s status as the world’s primary reserve currency are eroding more quickly than expected. What happens if the tower starts to collapse?

US dollar dominance: Playing Jenga with the global monetary system

We cannot ignore the dominant themes impacting markets across the world, but a resilient and supported European marketplace is well placed to prosper in these challenging times.

Resilient European High Yield market looks beyond tariff uncertainty

Securitised assets in the US offer diversification benefits and attractive yields for its high quality nature. When blended into LDI portfolios there is opportunity to enhance collateral waterfall resilience while improving risk and return dynamics.

LDI focus: Diversification benefits of US securitised credit

An overview on what ABS are and how the mechanism actually works.

US asset-backed securities: the basics

Important information: For use by professional clients and/or equivalent investor types in your jurisdiction (not to be used with or passed on to retail clients). For marketing purposes. This document is intended for informational purposes only and should not be considered representative of any particular investment. This should not be considered an offer or solicitation to buy or sell any securities or other financial instruments, or to provide investment advice or services. Investing involves risk including the risk of loss of principal. Your capital is at risk. Market risk may affect a single issuer, sector of the economy, industry or the market as a whole. The value of investments is not guaranteed, and therefore an investor may not get back the amount invested. International investing involves certain risks and volatility due to potential political, economic or currency fluctuations and different financial and accounting standards. The securities included herein are for illustrative purposes only, subject to change and should not be construed as a recommendation to buy or sell. Securities discussed may or may not prove profitable. The views expressed are as of the date given, may change as market or other conditions change and may differ from views expressed by other Columbia Threadneedle Investments (Columbia Threadneedle) associates or affiliates. Actual investments or investment decisions made by Columbia Threadneedle and its affiliates, whether for its own account or on behalf of clients, may not necessarily reflect the views expressed. This information is not intended to provide investment advice and does not take into consideration individual investor circumstances. Investment decisions should always be made based on an investor’s specific financial needs, objectives, goals, time horizon and risk tolerance. Asset classes described may not be suitable for all investors. Past performance does not guarantee future results, and no forecast should be considered a guarantee either. Information and opinions provided by third parties have been obtained from sources believed to be reliable, but accuracy and completeness cannot be guaranteed. This document and its contents have not been reviewed by any regulatory authority. Issued by Threadneedle Asset Management Limited, No. 573204 and/or Columbia Threadneedle Management Limited, No. 517895, both registered in England and Wales and authorised and regulated in the UK by the Financial Conduct Authority. Columbia Threadneedle Investments is the global brand name of the Columbia and Threadneedle group of companies. © 2025 Columbia Threadneedle. All rights reserved.

With inflation cooling and the US Federal Reserve transitioning from rate hikes to a cycle of rate cuts, bonds are poised to perform well in 2025. We believe success in the coming year will depend on how well portfolios are positioned to take advantage of lower rates while protecting against potential economic and credit volatility. In our view, the key theme in 2025 will be how investors successfully navigate greater dispersion across bond sectors.

Gene Tannuzzo Global Head of Fixed Income

“We believe the rate-cutting cycle should create a favorable environment for high-quality bonds in the US, particularly mortgage-backed securities and municipal bonds”

As we assess valuations, it appears the market is not yet fully pricing in the potential for significant credit weakness across the globe. Therefore, we think a cautious approach to credit is warranted. In addition, we expect credit dispersion will increase in 2025. While high-quality bonds are likely to perform well, certain industries are expected to experience elevated default rates – potentially in excess of 10% in certain sectors over the next two years, while others may remain closer to 1%. This divergence stems from the differing balance sheet health across industries, with highly leveraged companies – particularly in the high yield space – facing greater challenges. As economic volatility potentially rises, these weaker companies are more vulnerable to credit deterioration. This disparity creates an environment where active credit selection – our core strength at Columbia Threadneedle Investments – becomes essential for avoiding pitfalls and capturing the most attractive opportunities.

Navigating credit dispersion with active selection

So far, the Fed appears to have engineered a “soft landing”, with lower inflation accompanied by a gradual slowdown in growth. But it is important to remember that, historically, that’s how most hard landings begin. The challenge facing bond investors in 2025 will be whether the current economic deceleration continues smoothly or whether it evolves into a more severe downturn. The labour market will likely be a key factor. Should weakness in job creation persist, the economic outlook could deteriorate further. We think inflation will continue to decline towards the Fed’s 2% target, and that the Fed will ultimately lower rates to below the neutral rate of 3% by the end of 2025. This expectation is based on our view that there is more softness ahead in the labour market and consumer demand. However, two key factors could prompt the Fed to adjust its approach: Sticky or rebounding inflation: If inflation reemerges – particularly in core services – the Fed may need to pause its cutting cycle and stabilise rates in the 3%-4% range. A significant demand shock: A demand shock, especially coupled with labour market weakness, could cause the Fed to cut rates more aggressively, pushing them well below the neutral level, as seen in traditional rate-cutting cycles. Regardless of which path unfolds, the Fed’s roadmap for 2025 remains flexible, with incremental rate cuts expected to reflect evolving economic conditions.

Soft landing supports bond performance – but will it last?

Given our base case, we believe the rate-cutting cycle should create a favorable environment for high-quality bonds in the US, particularly mortgage-backed securities and municipal bonds. These sectors, which are already starting from attractive yield levels, are well-positioned to deliver strong price returns as rates decline. We are taking a slightly more defensive stance on corporate credit, given the current level of risk premiums. In the event of a harder landing, bond markets may experience increased volatility. High-quality and longer maturity fixed income securities are likely to benefit in such a scenario, as investors seek save haven assets during periods of economic stress. Globally, as the Fed aligns with other central banks that have already begun easing monetary policy – the European Central Bank and the Bank of England among them – asynchronous opportunities in European and Asian credit markets may also arise. Diverging economic conditions across regions may create valuable entry points for global investors.

Opportunities in a rate-cutting environment

Fixed income investors are entering 2025 with a strong foundation. With yields at attractive levels and the Fed in a supportive, rate-cutting cycle, bonds are well-positioned to generate healthy returns. Importantly, with the so-called “Fed put” – the belief that the Fed will intervene to support the economy during periods of stress – bonds are regaining their critical role as portfolio diversifiers. This implicit backstop should give investors confidence that even if economic conditions deteriorate, fixed income markets will remain supported. Encouragingly, a significant macroeconomic shift is not required for bonds to perform well. Starting yields are currently above their 20-year average in most sectors. The tailwind from falling interest rates will only further boost total returns.

Bottom line: bonds positioned for success in 2025

Return to home

“Third on the list of impossible things would be a TV personality winning the presidency of the United States in 2016 And again in 2024”

To prepare a presentation on what has changed for long-term investors during the past decade I dug out my notes from 2014. The results were sobering. In October 2014, macroeconomic factors were at the forefront of investor concerns. The International Monetary Fund (IMF) had forecast global GDP growth at 3.3% in 2014, following 3.3% in 2013. Not exactly exciting stuff. In 2014 a key consideration for investors revolved around the ongoing decline in US Treasury yields (the five-year note was around 1.5% in October of that year). For Central Bank FX reserves managers this led to a discussion on how best to diversify into higher yielding fixed income such as investment grade credit, public equites, and new currencies such as the renminbi. In 2014 we did not appreciate just how pivotal the year would be for geopolitics. In a cynical move just a few days after the closing ceremony of the Sochi Winter Olympics in the February, Vladimir Putin began his grab for Crimea. Annexation followed in March. Sanctions regimes were slowly mobilised after Crimea was annexed, and the election of Trump in 2016 facilitated a snowball effect of tariffs and counter tariffs (Figure 1).

Figure 1: The global backdrop – trade restrictions have risen sharply

We observe that the biggest drivers of financial markets in the past decade have been the impossible things that have overwhelmed our carefully considered medium-term quarterly economic forecasts. In 2014, investors might have considered the following six events as almost impossible to imagine: The most significant was the Covid-19 pandemic, a global health crisis that was predicted by nobody as it approached us – even though we know pandemics occur. We now have public deficit and debt numbers that were previously unimaginable. Russia’s invasion of Ukraine in 2022 triggered the most devastating war in Europe since the Second World War. The all-out invasion of Ukraine led to sanctions, disrupted supply lines and rapid increases in the price of gas and oil that boosted already increasing inflation rates. Third on the list of impossible things would be a TV personality winning the presidency of the United States in 2016 and again in 2024. In a world of frosty relations with China, Donald Trump was a willing actor when it came to taking the trade war to China and agreeing a policy of tariffs and sanctions.

Source: Global Trade Alert. *2024 extrapolated from September 2024 data

How do we break the spiral?

Next on the list would be President Xi of China engineering a job for life in 2018. The rollout of the Belt and Road Initiative began in 2013 when it was announced as a trade policy. Over the past decade it has taken on the appearance of an increasingly strategic geopolitical project. Trade and military alliances go together. The crisis in the Middle East will not have surprised many, but the Hamas incursion into Israel in late 2023 surprised everyone. Finally, don’t overlook Brexit. A local story, but one that opened the sores of populist and nationalist sentiment that have been bubbling in the UK for many years. The economic nationalism that ties all these events together has consequences. “Just in case” replacing “just in time” in global supply chains has implications for trade patterns and the price of goods. It will often mean paying more to ensure greater security of supply (ie a higher floor for CPI in future cycles). For FX reserves managers, who let’s not forget are government institutions, it may also have implications for constructing portfolios – ie building your friends into the asset allocation for what is effectively a national wealth portfolio, and perhaps having to choose which political bloc you want to belong to (for example, towards the US or, for some, towards China).

We can’t forecast unknown unknowns, but we can highlight known unknowns. In 10 years from now Iran’s supreme leader, Ali Hosseini Khamenei, will be 95, Putin will be 81 and Xi will be 82. Although North Korea leader, Kim Jong Un, will only be around 50, his health status is not clear. We predict that regime change in any or all of these countries is coming, but we don’t know what it will look like. This will be difficult for financial markets to price accurately and suggests that we will continue to see bouts of amplified volatility. When will the rubber band on fiscal policy – stretched like never before in 80 years – finally break? Led by the US, fiscal laxness argues for a higher floor for long rates in the longer dated future. Will bond investors refuse to buy, or will a first mover on fiscal consolidation enjoy a market response that eventually forces others to follow? Economic nationalism looks as though it is baked in. As we saw in the 1930s, tariffs and sanctions tend to lead to tit-for-tat responses, and a vicious spiral. It is very difficult to see how this problem can be defused, and it will likely be an important theme for the next decade. The question is how best to incorporate the theme into investment strategies. The argument is for a nimble approach to portfolio management. Periods of heightened market volatility will be an environment in which active management should beat passive. Investors should make their investible universe as wide as possible, utilise as many investment tools as their guidelines allow, and work with investment managers that have a strong track record.

What about the next 10 years?

Gary Smith Client Portfolio Manager, Fixed Income

“The extent of US dollar dominance will continue to erode due to the continued weaponisation of the currency”

The latest data from the IMF Currency Composition of Official Foreign Exchange Reserves (COFER) shows that the US dollar share of global foreign exchange reserves fell to 57.4% in Q3 2024. This is the smallest share since 1994 and represents a decline of almost 9% over the past decade (Figure 1).

Figure 1: US dollar share of global currency reserves on a downward trend (%)

The key driver of this has been a reaction to the increased “weaponisation” of the dollar. This has always been an aspect of the “exorbitant privilege” associated with the US dollar being the primary reserve currency . The country has been in the enviable and unique position of being able to use financial assets to achieve its foreign policy and (sometimes) military objectives without deploying soldiers. This has grown in importance since the 9/11 terror attacks (2001) and reached a recent peak in 2022 after the full-scale Russian invasion of Ukraine. Weaponisation will also be a driver of the next 10% decline in the dollar share. As early as 2017 the then US Treasury secretary Jack Lew acknowledged that the use of this weapon would push some players to avoid the dollar in the future, thereby reducing the extent of its dominance. We think that over the next 10 years another 10% will be eroded from the dollar weight within IMF COFER statistics, and if that happens 10 different currencies will benefit.

Source: IMF COFER, January 2025. Figures on a quarterly basis

The top 10 countdown

Over the past decade, it is the smaller currencies that have taken up most of the slack. Some of these such as the Japanese yen, UK sterling, the Australian dollar, the Canadian dollar and the Swiss franc are named in the IMF COFER report. All of them will continue to grow as the US dollar share declines (Figure 2).

A non-traditional currency we think will win is the South Korean won. It is named in the COFER report but is not measured individually, sitting in the “Other” category within the IMF data. It is this category that has made biggest gains in the past three years. Perhaps the IMF should publish more granular data? South Korea is economically and geopolitically connected. It is the 12th largest nation in the world in terms of GDP and is an important cog in the US association of like-minded nations. In May 2024 it emerged that South Korea was in discussions around joining the military security partnership between the US, the UK and Australia known as AUKUS . So, security agreements as well as trade flows (and the associated financial flows) underpin the argument for the won. A new name we think could appear on the list for the next decade is the Indian rupee. India is the world’s fifth biggest economy and its most populous nation. Size counts in this debate, as we saw a decade ago with the initial adoption and enthusiasm for China’s renminbi. India is “non-aligned” and keen to have cordial relations with a wide list of nations. Comparisons to the internationalisation of the renminbi are instructive. The Chinese currency began to be held as a reserve currency by central banks from 2010 onwards, despite a lack of currency convertibility. While not a substitute for deep, liquid and open capital markets, large FX reserves do help dampen currency volatility. And in the case of the rupee they may also provide comfort to global central banks looking to diversify their currency exposure. A bold forecast, but a small slice of this story will surely benefit the rupee.

The euro and renminbi will also win, albeit modestly

Source: IMF COFER, January 2025. Major reserve currency shares ex-US dollar and euro

Figure 2: The rise of ‘Other’ – currencies picking up the reserves slack

At the turn of the century the newly launched euro was expected to go toe-to-toe with the US dollar. Since then, the euro’s weight in FX reserves has barely changed. The lack of capital market union and failure to develop a single issuer bond market to rival the depth and liquidity of the US Treasury market are two reasons for this. Nevertheless, we think the euro, as the principal alternative to the US dollar, will take a small extra slice of the pie and remain in clear second place. The renminbi is currently home to around 2% of global FX reserves. We note that the share has declined since the Russian invasion of Ukraine. The renminbi story has also been hampered by capital market reforms that have fallen short of expectations, and most recently by Chinese bond yields that have fallen sharply. At current levels of yield, new buyers of renminbi bonds might be discouraged. However, geopolitical fracturing has two sides to it. For some nations China will be a friend rather than a foe, it will command a larger share of the trade flows with these nations, and the renminbi will appeal to the managers of those reserves. China is the largest trading nation for more than 120 countries and trading flows are potential payment flows for the renminbi. So, despite headwinds the yuan should continue to gain a modest FX reserves share over the next decade. Finally, the Singapore dollar should benefit. It already has a small slice of the FX reserves pie and could grow modestly from here. The currency should continue to ride on the coattails of the renminbi – large renminbi trade invoice flows through Singapore have led to rapid growth in the demand for Singapore dollar FX swaps. This will likely underpin future appetite.

The extent of US dollar dominance will continue to erode due to the continued weaponisation of the currency. But even if the weight of the greenback falls to 50%, we believe its primary dominance will be maintained because there will not be a single challenger from the pack. Instead, the next 10 years will see 10 currencies take a small slice of the next 10% wave of dollar erosion. We will also increasingly see the internationalisation of up-and-coming currencies as bond market reforms around the world improve and encourage access for foreign investors. This in turn should trigger an evolution of the leading global bond indexes. A convenient way for investors to position for these opportunities will be to invest in broad-based products benchmarked against emerging market and global aggregate indexes.

What it means for investors

Sources 1. OMFIF, Giscard d’Estaing: Architect of euro and sdr, 3 December 2020 2. Reuters, South Korea discusses joining part of AUKUS pact with US, UK and Australia, 1 May 2024 3. The Non-Aligned Movement (NAM) is a forum of nation states not formally aligned either with or against any major power bloc and is dedicated to representing the interests and aspirations of developing countries

1

2

3

“XXxxxxxxxx xxxxxxxxx xxxx xxxxxxxx x”

Alasdair Ross Head of Investment Grade Credit, EMEA

David Oliphant Executive Director, Fixed Income

Our fixed income team provide their weekly snapshot of market events

In Credit Weekly Snapshots

Download report

UK decay?

13 January 2025

A misdiagnosis of crisis

20 January 2025

Exit music (for a year)

6 January 2025

Long rally runnin’

27 January 2025

January 2025

Thanks given

2 December 2024

Égalité restored?

9 December 2024

It’s the end of the year as we know it

16 December 2024

December 2024

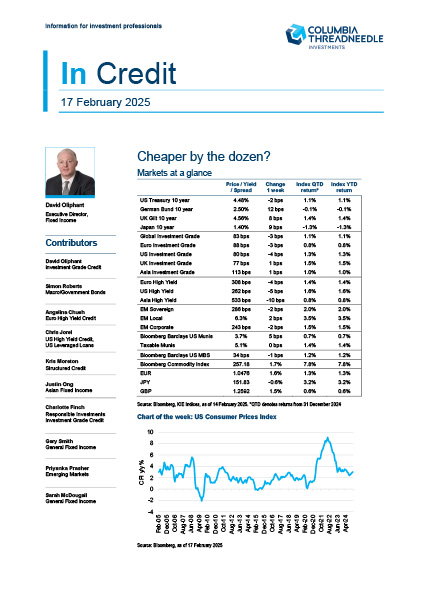

Cheaper by the dozen?

17 February 2025

Inflating inflation fears

24 February 2025

Trump, tariffs and trade tensions

3 February 2025

Higher for longer

10 February 2025

February 2025

Turkish fright

24 March 2025

A week of divergence

10 March 2025

Weakness abounds

17 March 2025

A lack of confidence

3 March 2025

March 2025

Tariff fears rattle risk markets

31 March 2025

Calm after the storm

28 April 2025

Liberated bears

7 April 2025

April 2025

Lower inflation but loss of top rating

19 May 2025

Easing trade tensions, rising risk markets

12 May 2025

May 2025

Rising conflict, rising oil prices

16 June 2025

Dazed and confused

2 June 2025

‘Take it to the limit' ...

9 June 2025

June 2025

“Fixed income returns will prove to be more dependent on starting valuations than a specific macroeconomic outcome”

Figure 1: Trending down - Wages continue to soften

Another important measure is the trimmed mean PCE, which excludes the highest and lowest values of the personal consumption expenditures (PCE) to focus on the core inflation trend. Both the one-month and six-month annualised rates of change indicate that we are moving in the right direction, similar to to pre-Covid levels (Figure 2).

Source: Federal Reserve Bank of Atlanta, as of 15 January 2025. The Atlanta Fed’s wage growth tracker is a measure of the nominal wage growth of individuals. It is constructed using microdata from the Current Population Survey (CPS) and is the median percent change in the hourly wage of individuals observed 12 months apart.

Importantly, data continues to show a slow but steady softening in the labour market. The quits rate, which indicates workers’ willingness to leave their jobs for better opportunities, is below 2019 levels (Figure 3), suggesting a less dynamic labour market. Additionally, the monthly average change in nonfarm payrolls has been declining each year, with no immediate signs of reversal.

Patience is the name of game

Source: Federal Reserve Bank of Dallas, as of 15 January 2025. The trimmed mean PCE inflation rate is an alternative measure of core inflation in the price index for personal consumption expenditures (PCE). It is calculated by staff at the Dallas Fed, using data from the Bureau of Economic Analysis (BEA).

Figure 2: Heading lower - Core inflation metrics continue to trend down

Given these observations, we believe inflation in the US will continue to move lower as the labour market continues to weaken. This, in turn, could prompt the Fed to cut rates more than the current forecast of two cuts in 2025. However, the impact of President Trump’s economic agenda remains a wildcard, with its precise effects on inflation uncertain. We believe the Fed’s approach to monetary policy in 2025 will be dictated by two risks. The first is the tail risk of the economy overheating, fuelled by a negative supply shock from tariffs and the immigration policy, plus a positive demand shock from tax cuts and higher fiscal spending. This combination could impede further progress on reducing inflation and bring the Fed’s easing cycle to an abrupt end. The second risk is that labour market trends continue, with wages remaining a weak passthrough into inflation. With inflation under control, the Fed can focus on adjusting policy to better support the slow but steady decline in the labour market. It is the former scenario that has dominated market sentiment in the early days of 2025, with intermediate and longer maturity Treasury yields rising uncomfortably close to cycle highs.

The year started with some sharp moves in fixed income, with developments in terms of inflation trends and labour market conditions. So, how does this align with our broader fixed income outlook for the year?

Should fixed income investors reposition given recent markets shifts?

The US Federal Reserve’s focus on a handful of indicators leading into December 2024 suggested that inflation in North America was becoming sticky. This concern has been on and off the table several times since last year. During the first quarter of 2024 the market got very worked up when the pace at which inflation was declining slowed. Inflation ultimately continued to trend lower, which enabled the Fed to cut for the first time in September. The moral of the story is that markets can be overly optimistic about the inflation trajectory one minute, and then not optimistic enough the next. Markets have a way of swinging to extremes like that.

Don’t overreact, we’re still moving in the right direction

One of the critical indicators is wage growth. Historically, wages have been a durable pass-through mechanism into inflation. When employers pay more to attract labour, they pass those costs on to consumers, creating a cycle of rising prices. Wage growth has been steadily declining for more than two years (Figure 1), and the Fed has acknowledged that wages are not fuelling inflation today.

What indicators suggest inflation will still move lower?

Source: US Bureau of Labor Statistics, Quits: Total Nonfarm [JTSQUR], retrieved from FRED, Federal Reserve Bank of St. Louis.

Figure 3: Quits rate also heading down - Labour market continues to soften

Katherine Nuss Fixed Income Client Portfolio Manager

FRB Dallas trimmed mean (1-month)

FRB Dallas trimmed mean (6-month)

Jan 2019

Notably, while we have a view on how inflation and the labour market will evolve, we think fixed income returns will prove to be more dependent on starting valuations than a specific macroeconomic outcome. For example, fixed income yields are generous today because the risk-free rate has risen, not because credit spreads are wide. Higher risk-free rates – and real yields specifically – suggest that investors are being more appropriately compensated for the risks of stronger growth, greater inflation uncertainty, and/or rising fiscal deficits. In contrast, credit spreads remain near their tightest levels since the 2008 global financial crisis. This creates asymmetric risk that spreads could move wider, which would erode returns relative to duration-neutral Treasuries. As such, we see better value in duration risk – not because we are betting on the Fed, but because we are receiving better compensation relative to the risk. So, the name of the game for 2025 is patience. We do not know exactly when the turning point will come, but we are positioned to make the most of elevated yields while mitigating potential downside from widening spreads by focusing on higher quality opportunities in shorter maturities where prices historically demonstrate less volatility.

Atlanta Fed's wage growth tracker (%)

Trimmed mean personal consumption expenditures (%)

Quits rate (%)

“Monetary policy and valuations are headwinds for further spread tightening, but fundamentals remain broadly robust”

Figure 1: US dollar rate expectations

Elevated interest rates also reduced money supply by making access to credit more expensive. Quantitative tightening (QT), the unwinding of quantitative easing, was also removing liquidity from the financial system. These policies were aimed at bringing inflation back to target. With inflation now closer to 2% (Figure 2), we have seen an easing in these policies including a rebound in money supply and a slow-down in QT.

Source: Bloomberg and Columbia Threadneedle Investments, January 2025

By increasing interest rates, central banks pushed real yields (nominal interest rates minus inflation) above long-run averages from very depressed levels. As inflation started to fall, central banks were able to pivot to a rate cutting cycle, keeping real rates at or just above their long-run averages of around 2% in the US and 0.25% in Europe. If inflation continues to fade, central banks should be able to continue cutting rates. This is due to the fact that if they keep rates unchanged, real yields would actually drift higher into a slowing growth and falling inflation environment – pushing even harder on the brakes as the economy slows. Although monetary policy has eased over the past six months as inflation has slowed, we believe it remains in restrictive territory (rates above the neutral rate and real yields at long-run averages). Our base case is for US inflation to continue to decline towards the Federal Reserve’s 2% target, and that the Fed will ultimately lower rates to below the neutral rate (we estimate around 3%) by the end of 2025. This is based on our view that there is more softness ahead in both the labour market and consumer demand. We identify two key risks to this view: first, sticky or rebounding inflation, particularly in core services, could prompt the Fed to pause their cutting cycle and stabilise rates in the 3%-4% range. Secondly, a demand shock – especially if coupled with labour market weakness – could cause the Fed to cut rates more aggressively, pushing them below the neutral level, as seen in traditional rate-cutting cycles. To read more about the importance of credit dispersion and quality click here

Source: Macrobond and Bloomberg, December 2024

Figure 2: Inflation on a downward trend

Fixed Income Desk Investment Grade Team

Despite an eventful year for geo-politics, inflation and central banks, credit markets remained robust, supported by the all-in yield and strong credit fundamentals. Having seen a rally in credit spreads across regions and sectors since the post--Covid wides of late 2022, this year could see more dispersion. Our investment grade outlook starts by assessing where we are in the cycle with a focus on fundamentals (economic and corporate), valuations and technicals (investor sentiment, demand and supply dynamics etc). Currently, we assess monetary policy conditions and valuations as being headwinds for further spread tightening, but importantly fundamentals remain broadly robust. We acknowledge that a potential rebound in mergers and acquisition activity after a slow 2023 and 2024 could be a risk to our stable credit fundamental outlook.

In addition, potential deregulation in the US could further challenge that base case. The combination of slowing global growth, an uncertain geopolitical backdrop, moderately restrictive monetary policies and rich valuations reduce the ability of the asset class to absorb external shocks or policy error. Valuations have moved a long way since the wides in 2022, but it is important to note that credit spreads can spend an extended period of time below their longrun average and median levels. However, given the asymmetry of the asset class the upside is increasingly limited. Consequentially, we have reduced the overall credit risk in our funds – close to neutral – but the solid supply/demand backdrop and corporate fundamentals keep us from having a more negative outlook. A new terminal interest rate means a new environment for companies and investors to navigate. The rate cutting cycle should create a favourable backdrop for IG bonds, but we think a bigger theme for 2025 will be credit dispersion. Reflecting this, we have increased credit quality in terms of sectors and moved up the capital structure, as well as positioning more defensively.

Over the course of the past six months inflation has continued to cool, allowing central banks to pivot to a rate cutting cycle. Global financial markets are expecting more cuts in 2025 (Figure 1). However, the timing and size of those cuts is being challenged by political uncertainty.

Macro backdrop

“If the dollar begins to weaken and yields decline, it suggests market participants believe countries will lower their trade barriers, increasing global trade”

Smaller drop in Treasury yields following 2024 rate cuts relative to previous cycles

One way to lower the cost of debt (in this case Treasury yields), is to improve the creditworthiness of the underlying business (the US government). Recent headlines suggest that President Trump is attempting to do this by reducing the US budget deficit. In terms of spending, there’s an effort to cut costs by applying zero-based budgeting to the US government. In terms of revenue, there’s a focus on stimulating the economy by reducing the price of US goods abroad, thereby increasing US exports.

Source: Bloomberg LP and Columbia Threadneedle Investments, as of 31 January 2025

Why are we watching Treasury yields?

We believe President Trump is focused on yields and is seeking alternative ways to lower interest rates given the weaker relationship between the federal funds rate and Treasury yields in this current cutting cycle. So far, 2024 rate cuts have had less of an impact on Treasury yields and the cost of borrowing for individuals and businesses than any other recent rate cutting cycle.

Tariff headlines continue to drive significant market volatility, with the potential long-term effects of the Trump administration’s proposed and imposed tariffs yet to be fully understood. As we attempt to separate the noise from the lasting impact of tariffs, we will be watching the direction of the US dollar and Treasury yields. Broadly speaking, the current tariff framework includes two types of tariffs: First-mover tariffs are designed to increase the cost of goods imported into the US from abroad. This kind of tariff could raise the risk of higher inflation as it will prove to be a price shock that companies will attempt to pass along to consumers. Higher inflation expectations will likely drive Treasury yields higher and push out market expectation for additional Federal Reserve (Fed) rate cuts. Longer term, if the US dollar and Treasury yields begin to fall, it could suggest that tariffs are impacting demand and slowing the US economy. Reciprocal tariffs are designed to mirror the level of tariff imposed on US goods imported into other countries. One potential reason for threatening to impose identical reciprocal tariffs is to force other countries to reduce their tariffs on imported US goods. If the strategy proves effective and tariffs on US imports are lowered, consumers in those countries will perceive US goods as less expensive. Assuming all else is equal, this could boost demand for these goods, thereby increasing US exports and reducing the US trade deficit, which might lead to a weakening of the US dollar. We would subsequently expect Treasury yields to fall and inflation pressure to ease, reflecting greater global competition, a flatter trade balance and more room for the Fed to lower rates.

Move beyond the headline noise to assess the investment implications

Michael Laskin Senior Analyst, Fixed Income

Michael Guttag Senior Equity Portfolio Manager

Net change in yield following the Fed's first rate cut (percentage points)

Tariff headlines are coming in quick and fast. In the case of first-mover tariffs, if we see a stronger US dollar and higher yields it could suggest higher inflation in the near term, a risk of long-term demand destruction, and a higher risk of a recession. In the case of reciprocal tariffs, if other countries retain their existing levels of tariffs on US imports and the US increases its tariffs in response, we expect similar outcomes as in the case of first-mover tariffs. However, if other countries lower their tariffs on US imports in response to the threat of reciprocal tariffs, we would expect a weaker dollar and lower yields, reflecting a reduction in the US deficit and an increase in global trade For investors, it’s important to focus on the impact these policies could have on the economy and the market. As active managers, we are closely monitoring the US dollar and Treasury yields, and leveraging our central research capabilities to proactively position portfolios ahead of these policy risks.

The bottom line

As with first-mover tariffs, we believe that reciprocal tariffs may provide an indication of potential impact through the movement of the US dollar and Treasury yields. If the US dollar continues to strengthen as these tariffs are announced, it would suggest market participants believe higher tariffs will be the final outcome. However, if the dollar begins to weaken and yields decline, it suggests market participants believe countries will lower their trade barriers, increasing global trade.

Days following first Fed rate cut

“Although the desire to move away from the weaponised dollar is real and growing, the switch will be tough”

Many nations would like to reduce their dependence on the increasingly weaponised US dollar, especially for dollar-denominated trade that does not pass through the US. The idea of a shared currency issued by the BRICS nations (Brazil, Russia, India, China and South Africa) made headlines in late 2024 ahead of their October conference in Kazan, Russia. Wanting to move away from the dollar is understandable, but making progress will be challenging. Here are eight questions for proponents of a BRICS currency.

Not quite. Brazilian president, Luiz Inácio Lula da Silva, has expressed enthusiasm for the idea of a new currency for settling trade between the BRICS nations. However, politicians from South Africa, India and particularly China have been conspicuously quiet on the topic. The BRICS nations are not a homogenous group with a common set of aims. These nations are diverse with differing objectives and, in the case of India and China, significant rivalries. This is not an obvious starting point for a shared currency project.

1. Is this a Russian dream to dodge US sanctions?

Settlement in local currencies is increasing, albeit from an extremely low level. However, the scope is constrained by nations having a limited appetite for accumulating the currency of the other. For example, since sanctions were imposed on Russia in 2022, oil exports have been redirected to India. However, Russia does not want to accept rupees because of a limited demand for Indian exports. Local-to-local trade in home currencies will be easiest between nations where trade is in balance – but that is rare. A solution to the rupee conundrum was found by using the UAE dirham, a currency fixed to the value of the dollar and internationally accepted in multilateral trade. The BRICS nation currency that has made the most progress in terms of increased usage in international transactions is the Chinese renminbi. As a nation that is the largest trading partner for 120 other nations it is best positioned to become the de facto BRICS currency.

6. Why not just use local-to-local currency settlements for intra-BRICS trade?

It is not clear if the plan is to replace domestic currencies or create something to operate in parallel. The lack of clarity on this seminal point is an indication that discussions are at an early stage. These things take time. The euro was created in 1999, 29 years after the 1970 Werner report proposed a single currency, and 21 years after the launch of the European Monetary System. The eurozone was built on shared political institutions and 50 years of economic integration among neighbouring countries. A ‘big bang’ move to a shared currency for the BRICS nations is not practicable. A fixed but adjustable exchange rate regime might be a more viable route to a new currency.

2. Would it replace domestic currencies?

The experience of the European Exchange Rate Mechanism (ERM), a precursor to the euro, is instructive. The system had a bumpy history but eventually succeeded in establishing guide rails for the launch of the single currency. Fixed but adjustable exchange rates require occasional realignments to account for differing inflation rates over time. Under the ERM, the burden of adjustment usually fell to the nation of the weaker currency. Realignments tended to be fraught events with political repercussions. If a BRICS currency ran parallel to domestic currencies, who would manage exchange rates versus the domestic currencies? Lula’s suggestion for an inter-BRICS trade currency redenomination out of the dollar would require similar adjustments. The weights of each currency would need to constantly be adjusted to reflect global currency movements (often versus the dollar) and prevent arbitrage.

3. How would such an exchange rate system work?

Attempting to establish a BRICS currency among the current members would be an enormous undertaking; the recent initiative to expand the group – with invitations sent to the United Arab Emirates, Iran, Indonesia, Ethiopia and Egypt among others – would only add to this complexity and reduce the probability of a new currency arrangement. If the BRICS group is intended to provide a counterweight to the US-led Bretton Woods institutional framework, which led to the creation of the International Monetary Fund and the World Bank, it should be highlighted that Ethiopia and Egypt are currently reliant on IMF financing. Will the BRICS group be offering a more credible alternative financing mechanism?

4. Would expanding the list of ‘BRICS’ nations enhance the appeal of a shared currency?

A gold-backed currency might appeal to major gold producers like China, Russia and South Africa. If a gold-backed currency replaced domestic currencies, then the BRICS nations would find themselves on a version of a gold standard. Gold-backed currency regimes in the 20th century collapsed because governments needed to print currency to pay for war (the first world war for European nations and the Vietnam war for the US). Does Russia understand it might have to rein in military spending to maintain a peg? In addition, how would responsibility for maintaining convertibility into gold work between a disparate list of nations with differing holdings of gold and access to new production? If ‘goldbacked’ meant convertible into gold at the prevailing market price, then the unit would change in value every day. Who would intervene and defend when one of the underlying currencies fell in value? Would a gold contribution be required by the nation of the weak currency at a time of vulnerability? Such a system would lead to destabilising speculative movements of gold between participant countries – the opposite of the desired stable and predictable framework.

5. Would a gold-linked currency be more viable?

The Russian delegate to the BRICS summit recommended a common platform for cross-border payments using central bank digital currencies (CBDCs). This would avoid having to use the dollar, the US banking system and Swift, the interbank payment service. However, the roll-out of CBDCs is best described as a ‘work in progress’. The Bank for International Settlements has helped to develop a platform, known as ‘Project mBridge’, with the participation of five central banks including the People’s Bank of China . It is a solution for the long term, but it could eventually provide for own-currency settlement using CBDCs. Although it would not address the problem of trade imbalances leading to piles of unwanted local currency, it could lead to much lower transaction costs, which might tip the scales for some players.

7. What came out of the Kazan summit?

As it stands, Trump is reacting to a problem that does not exist and is unlikely to become one during the four years of his presidency. However, historian and economist Barry Eichengreen, from the University of California, Berkeley, has labelled the BRICS currency idea ‘a charade’ , which certainly makes it sound more like a basket case than a currency basket.

8. Why is US president Donald Trump warning against a BRICS currency?

Although the desire to move away from the weaponised dollar is real and growing , the switch will be tough – even for trade flows that occur within the BRICS group. The power of incumbency is strong. At the margin there will be a bigger role for the renminbi and for gold. However, the asset management industry is unlikely to need to provide BRICS currency-linked products for several decades. Traditional core fixed income products such as global aggregate, developed market governments, and hard currency emerging market debt will continue to be the bedrock for fixed income investors.

“A fixed but adjustable exchange rate regime might be a more viable route to a new currency”

Sources 1. BIS, Project mBridge reached minimum viable product stage, 11 November 2024 2. Project Syndicate, The BRICS Currency Charade, 14 November 2024 3. Columbia Threadneedle Investments, FX reserves and the 10-10-10 proposition, 21 January 2025

“The impact of a ceasefire on Russian oil exports is expected to be minimal, as production will likely be determined more by OPEC+ quotas than by sanctions”

The Trump administration has initiated talks with Russia on a broad range of security issues, including a potential ceasefire agreement. These developments could have significant geopolitical and economic implications. It is important to emphasise that the process remains fluid – at times an agreement may seem imminent, while at others, negotiations appear to stall. We believe there are two main scenarios to consider regarding the investment implications of a potential ceasefire. Our base case is for a limited ceasefire, while the more bullish case is for a sustainable peace deal between Russia and Ukraine. We explore both scenarios below, focusing on the investment considerations, particularly as it relates to Russian sovereign and corporate debt, emerging market debt, and the energy sector.

Assessing the potential opportunities and challenges

Our cautiously optimistic base case is for a limited ceasefire in Ukraine, which would involve a small peacekeeping force but no security guarantees from NATO or the US, and conditions requiring Ukraine to hold elections before Russia agrees to talks for a more lasting peace deal. In this case, as the possibility of a ceasefire gains traction, the US and Europe may lift financial sanctions imposed on Russia when it invaded in 2022. It is important to note that sanctions will likely only be lifted if there is a ceasefire, although comments from the US suggest this sequencing is up for debate. If US sanctions are lifted, and investment in Russia securities permitted, we believe the most immediate market impact would be on Russian sovereign debt, with current prices offering significant discounts to emerging market peers. Russian corporate credit could also present attractive investment opportunities. However, it is important to note that credit ratings across the Russian market are unlikely to return to investment grade due to qualitative factors. Furthermore, investors and ratings agencies will have to determine how to treat the cash paid into domestic Russian bank accounts that has been servicing these bonds since sanctions were enacted. There might also be opportunities in Ukraine’s hard currency debt, although this depends on the nature and conditions of the ceasefire. Other emerging market beneficiaries could include the hard and local currency bonds of both Turkey and Egypt. Turkey could benefit from stronger European economic growth and lower gas prices, while Egypt could benefit from lower wheat prices.

Base case: A limited ceasefire

In the more bullish but less likely scenario of a sustainable peace agreement with meaningful Russian concessions, Europe could also lift energy sanctions that would allow for a partial resumption of gas flow through the Ukraine pipeline to Europe. This development could help lower energy prices in Europe. In the base case scenario, we think it is unlikely for European energy sanctions on Russia to be lifted quickly. In terms of Russian oil exports, the impact of a ceasefire is expected to be minimal in either of the scenarios, as production will likely be determined more by OPEC+ quotas than by sanctions.

Bullish case: A sustainable peace deal

While the path is uncertain, a potential ceasefire could bring some respite to the region and could also have significant geopolitical and economic implications. The market is likely to price in developments quickly, even if it takes several months to ultimately lift sanctions and resume Russian pipeline gas flows to Europe. We continue to closely monitor events as they unfold.

“Our cautiously optimistic base case is for a limited ceasefire in Ukraine, which would involve a small peacekeeping force but no security guarantees from NATO or the US”

The removal of sanctions on Venezuela in 2023 serves as a helpful example to understand the potential timeline and impact of sanctions removal on asset prices. In Venezuela, sovereign bond prices doubled from $10 to $20 the day after sanctions were removed in October 2023, and then peaked a couple of months later in January 2024 at $23. Subsequently, J.P.Morgan announced index reinclusion in February 2024, which was phased in over three months from April to June 2024. During this period, prices ranged between $18 and $22 before domestic politics took over as the driver of price action. It is important to note that Russian bonds are currently not trading at comparably distressed prices given their stronger underlying credit fundamentals.

The Venezuela precedent

Source: Bloomberg, as of 28 February 2025. An investment cannot be made in an index

Impact of lifting sanction on Venezuelan bonds

J.P.Morgan Emerging Market Bond Index (Price, $)

Secondary sanctions lifted

Index inclusion announced

Index inclusion period

Adrian Hilton Head of Emerging Market Debt

Gordon Bowers Research Analyst, Emerging Markets

“The market outlook is for more volatility in bond yields, curve shapes, cross-market spreads and currencies”

Geopolitical shockwaves have arrived at surprising speed in recent weeks. The consequence of US president Donald Trump’s decision to halt financial and military support for Ukraine, coupled with a warning that the burden of providing a military shield for Europe would cease to be a job for the US, has marked an inflection point and triggered a bold response from Europe. The German federal elections in late February took place against an expectation that German fiscal policy would be loosened. But the extent of the proposals from incoming chancellor Friedrich Merz are far larger than expected. Echoing Mario Draghi from 2012 , Merz stated that Germany would do ‘whatever it takes’ to fend off ‘threats to freedom and peace’ in a discussion around European self-sufficiency in the provision of military defence, following 80 years of relying on a US shield. The proposed plan also includes a €500 billion infrastructure fund aimed at enhancing Germany’s infrastructure and stimulating economic growth. To finance this initiative, Merz is attempting to amend Germany’s constitutional ‘debt brake,’ which traditionally limits new borrowing. The proposed amendment would allow defense spending exceeding 1% of GDP to be exempt from these borrowing constraints, effectively enabling unlimited borrowing for defense purposes. The outcome could have profound implications for Germany’s economic and defense policies in the coming years.

All of these market moves have been of great interest to the global rates desk at Columbia Threadneedle Investments, and in particular our global aggregate strategies. The market outlook is for more volatility in bond yields, curve shapes, cross-market spreads and currencies. But with turmoil comes opportunity. Now is the time for active managers with a proven track record in the global aggregate space.

Source: Bloomberg, as of 26 March 2025

If the package is passed by the Bundestag, it would be the largest fiscal boost in 80 years – larger, even, than that associated with reunification. It is not just Germany that is flexing its spending. European Commission president, Ursula von der Leyen, has proposed an escape clause for nations in danger of breaching the Stability and Growth Pact to allow them to increase their defence spending without triggering an Excessive Deficit Procedure (such a move was enacted during the Covid-19 pandemic when the European Union (EU) suspended its budgetary rules). She also announced common EU bond issuance for defence spending, and a call for more funding for the European Investment Bank is expected. There is even talk of a new bank for European rearmament that could include Norway and the UK, which would become a vehicle for military-specific bond issuance. The market reaction to the proposals has been enormous. The government bond market has priced a once-in-a-lifetime shift in policy regime, and the jump in the 10-year bund yield of 30 basis points on 5 March was the largest single-day rise since German reunification was announced in 1990. Additionally, we saw the biggest three-day jump in the value of the euro for a decade, while interest rate swaps traded at -29bps versus 10-year bunds – a level not seen the early days of the Eurozone crisis in 2010. The difference between the German 30-year yield and the two-year yield has doubled since the start of the year (back to levels last seen when the European Central Bank had negative official interest rates) on the expectation that increased future issuance will tend to be at the longer end of the yield curve (Figure 1).

German 2s/30s yield curve steepening

German yield curve steepener – as the burden on issuance is expected to be at the long end of the curve. Cross market underweight Germany versus US – as the market viewed much greater fiscal stimulus in Europe relative to the US. Euro swap spread tightener – as government issuance is expected to increase relative to corporates. All three of these positions worked individually, but through using a risk-adjusted framework a combination of these positions was more optimal.

What trades benefitted in this environment

Sources 1. When president of the European Central Bank, Draghi vowed to do ‘whatever it takes’ to prevent the euro from failing during the Eurozone crisis. 2. The Stability and Growth Pact is a set of rules designed to ensure EU countries pursue sound public finances and coordinate fiscal policies.

“May you live in interesting times”

- widely accredited apocryphal Chinese curse.

“As credit spreads have widened, pockets of opportunity have emerged in sectors with less exposure to trade and growth risks”

A nimble strategy will be crucial for investors bracing for a fluid economic landscape marked by growth headwinds, policy shifts, and intense scrutiny of the Federal Reserve's next steps.

Global capital markets have seen a noticeable shift in expectations this year. Although backward-looking economic fundamentals still look solid – unemployment is low, inflation has moderated and corporate fundamentals are generally strong – investors are feeling more cautious. The optimism that peaked following the US election has given way to concerns over downside risks to growth. Markets have responded to this shift with equities struggling, credit spreads widening and Treasury yields falling.

Figure 1: What’s driving market volatility?

Several factors have shaped bond market performance so far this year:

Source: Federal Reserve Bank of San Francisco, as of 31 March 2025. The Daily News Sentiment Index is a high frequency measure of economic sentiment based on lexical analysis of economics-related news articles. Higher values indicate more positive sentiment and lower values indicate more negative sentiment.

Drivers of bond market returns

Entering 2025, investors expected pro-growth policies (deregulation and tax cuts) to take centre stage. Instead, the focus has been on tariffs and tighter immigration policies – both of which could weigh on growth. The US Federal Reserve (Fed) has also acknowledged that risks are skewing to the downside.

Changing expectations (Daily News Sentiment Index)

What’s next for the Fed and rates?

Source: US Federal Reserve, as of 31 March 2025.

Figure 2: Fed participants signal heightened downside risks

Projected risks to GDP growth (Number of Fred board participants)

As investors grapple with these challenges, fixed income has regained its traditional role as an effective portfolio diversifier. In this environment, a focus on high-quality bonds and selective credit exposure is essential.

Softer US growth expectations: Economic growth in 2024 was solid, but concerns are rising about headwinds in 2025. Geopolitical risks, policy uncertainty and weakening business and consumer sentiment have shaken investor confidence. Inflation uncertainty: While the inflation surge of 2022 has largely faded, the potential impact of new tariffs looms large. With recency bias likely playing a role, investors are wary of a scenario where inflation reaccelerates, which could keep the Fed on hold longer than currently expected. Government spending and pro-growth policies outside the US: The US bond market typically drives bond yields globally, but in recent weeks global developments have been impacting US markets. Notably, expectations for fiscal stimulus and other pro-growth policies in Germany and Japan have exerted upward pressure on US rates.

• • •

So far this year, credit has underperformed duration. Despite this weakness, credit markets have remained orderly, with buyers stepping in to capitalise on improved valuations. Today’s modestly wider spreads reflect lower Treasury yields rather than outright weakness in corporate bond prices. As expected in this environment, high-quality fixed-rate debt has outperformed high-yield, bank loans and other floating-rate instruments. Overall, however, credit is still fairly expensive by historical standards. A surprising source of outperformance, relative to expectations at the beginning of 2025, has been emerging markets. Investors in emerging market debt have already navigated similar tariff policies during the previous Trump administration, and risk premiums were built in last fall. Importantly, tariff discussions have been equally focused on developed market trading partners like Europe and Canada as they have been on emerging market economies like China and Mexico.

The Fed held rates steady at its latest meeting but announced a slowdown in the pace of its quantitative tightening program. This suggests a subtle shift toward easing, even if rate cuts aren’t imminent. The Fed faces a tricky balancing act. Tariffs could push inflation higher, but they could also hurt growth by reducing consumer spending and business investment. This interplay adds another layer of complexity to the Fed’s decision-making process. The Fed has indicated that it remains open to cutting rates twice this year. Before committing to a path, it will likely need to see clearer signs of how the potential tug of war between rising inflation and weakening demand will play out.

As credit spreads have widened, pockets of opportunity have emerged in sectors with less exposure to trade and growth risks. Security selection will be important here, as certain industries – such as autos and building materials – face greater pressure from tariffs and supply chain disruptions, while others, like chemicals and some consumer sectors, may hold up better. We think dispersion within the high-yield market is likely to grow, and credit selection will be a significant driver of returns. One of the key themes this year is the return of fixed income as a portfolio diversifier. Unlike recent years, when bonds struggled to provide downside protection, high-quality fixed income has reasserted its role as a volatility buffer. With equity markets facing ongoing uncertainty, this dynamic is likely to remain in focus.

Positioning portfolios in this environment

Investors should be prepared for a fluid economic outlook as the year unfolds. Growth concerns are rising, policy uncertainty remains high and the Fed’s next moves will be closely scrutinised. In this environment, a nuanced, diversified approach to portfolio construction will be essential.

-0.12

Weighted to upside

Broadly balanced

Weighted to downside

0

4

6

8

10

12

14

16

18

Dec 2024

Mar 2025

“Without first fixing the engine, by recapitalising the sector, stimulus will only make the financial system more unstable”

With delinquent loans from the global financial crisis still sitting on its books, we don’t think the conditions are right for China to repeat its stimulus trick for a third time. The size of the tariffs placed on Chinese imports to the Unites States is changing week to week. Despite the recently agreed 90-day moderation, the potential effect on Chinese economic growth could be meaningful . This comes at a time when China seriously needs to improve domestic demand and consumption . Meanwhile in Europe, Germany has torn up the rulebook with an extraordinary fiscal stimulus announcement that will help combat the impact of tariffs placed on its exports. China has a track record of stimulating its way out of trouble, with enormous packages announced in 2008-09 and again in 2015-16. It has modestly loosened policy this year, but will China once again stomp on the stimulus gas pedal? Don’t count on it. For while Germany’s engine is newly serviced and ready to go, China’s engine is all clogged up and in need of a rebuild.

Figure 1: China surges ahead - Size of banking sector ($trillions)

Source: CEIC / US Federal Reserve / ECB / Autonomous data, as of January 2025.

These bad loans aren’t new; China just hasn’t dealt with the legacy of the previous two credit binges. We estimate that around half of the delinquent loans written following the global financial crisis (GFC) are still on bank balance sheets today. The system has simply not cleared. If all the losses were recognised today, the small and medium-sized banks would be insolvent (at least by Western regulatory standards). When banks get cleaned up, losses must be recognised and fresh capital raised. Take Japan in the 1990s and the US in the 2000s: Both systems had to book impairment charges over time of about 10% of loans . We estimate China has a similar amount still to deal with. The US did it quickly, over a three-year period following the GFC. In Japan it took about 15 years, with authorities spending the first seven years hoping growth would return to resolve the problem. China is going down the Japanese route. The regulator has removed the requirement for any loan loss provisioning on the riskiest loans until the end of 2027 . The loans may have gone bad, but everyone is being encouraged to pretend they haven’t. If the Chinese banks start to provision in 2028, the system might clear in 2035.

Paul Smillie Senior Credit Analyst, Investment Grade

Since the first big stimulus in 2008, the Chinese banking sector has grown by $50 trillion, going from around 2x nominal GDP to around 3.2x . China now has the largest banking sector in the world by some margin (Figure 1). This has been driven by growth in the country’s shadowy, poorly regulated small and medium-sized banks. When credit grows much faster than nominal GDP, bad loans build up in the system. Often, as with China currently, problems show up in property lending. Indeed, every time a banking sector has seen this sort of growth, it has ended badly . A reasonable estimate for the latent losses in the Chinese system is about $4 trillion . For context, that is equivalent to the combined loan books of Bank of America, Citigroup, JP Morgan and Wells Fargo .

What exactly is China’s problem?

We should point out that lots of good work has been done by the Chinese authorities. There has been a slow hidden digestion of the problem over the past five years, with about 1% of the loan book written off each year. In addition, some government capital was recently earmarked for the big state banks . That has been enough to stop things getting worse, but not enough to eat away at the stock of bad loans. The system needs a big recapitalisation, which cannot be done behind the scenes. It requires the authorities in China to admit there is a problem – something that is politically deeply unpalatable .

Why hasn’t China fixed the problem sooner?

Yes and no. Credit needs to keep expanding for China to hit its growth targets. If earnings were channelled into recognising bad debts and not into building capital to support loan growth, credit growth would have to slow materially, from 10% to less than 5% . Authorities cannot let that happen either.

Can the banks increase loan loss recognition?

It’s not that straightforward in China. The German fiscal stimulus will be paid for with funds borrowed on the international capital markets. Yes, the local banking sector will buy some of the debt, but it will also go to investors all over the world. The interest rate at which Germany can borrow will be set by the market. In China, the government borrows almost exclusively from the banking sector, which is mostly state owned. This allows the government to set its own borrowing cost. It also means that as the government fiscally stimulates, the banking sector balloons. What’s more, the borrowing is typically not from central government coffers but from local government (entities such as local government financing vehicles, about which little is known). This doesn’t tend to get paid back, which ultimately means we end up with even bigger banks with yet more bad debt. Pumping the credit pedal again might add back a few much-needed percentage points to GDP growth in the short term, but it will create a bigger problem with the banks in the longer term. Without first fixing the engine, by recapitalising the sector, stimulus will only make the financial system more unstable.

Can the government borrow and leave the banks out of it?

All the above would, of course, matter a lot in the West. Funding providers would run for the hills for fear of having investments in an insolvent bank. It would be terrible for GDP growth, as it has been on many occasions in the past (take Ireland and Spain in the early noughties, for example) . However, the question we must ask is: Does it matter in China? There are good reasons why it doesn’t: All the lending is in local currency and the capital account is closed, meaning there is no chance of a classic emerging market crisis where foreign currency funding is pulled, banks fall over, and a currency crisis ensues. (This is what happened in the Asia crisis.) Plus, the banking sector is state owned, and if China did recognise all the losses all at once, the total bill for the sovereign would be about 20% of GDP . China can probably afford that.

Does it matter?

Not quite. It goes back to how big the banking sector is, but this time let’s compare it to currency reserves. Over the past decade China’s currency reserves have remained steady, hovering around $3-$3.5 trillion, while the banking sector has doubled in size to $60 trillion. That means there is the equivalent of $60 trillion of liabilities (or funding) in the Chinese banking system. If Chinese depositors were to begin to lose faith in China’s financial stability, they could try to move money out of the country and put it into US dollars. It would only take a small proportion of the $60 trillion banking sector liabilities moving to make a big dent in the $3 trillion currency reserves . Declining reserves could in turn leave China with a currency problem . Of course, China prevents that money from leaving the local system via tight capital controls, but it is possible – especially for corporates involved in international trade – to get money out. It is this risk, we believe, that is making the Chinese authorities think twice about turning on the stimulus taps. Instead, we think the government will focus on targeted ways to encourage local depositors to funnel those funds into consumption.

Nothing to worry about then?

China might be tempted to follow Germany and get the stimulus bazooka out, but a broken banking sector makes it a high-stakes gamble. We are not doomsayers about China. We believe the Chinese authorities will continue with a pragmatic approach focussed on domestic consumption growth over the longer term. That means a policy of targeted, piecemeal stimulus. And if that is not the path taken – keep an eye on the currency.

Sources 1. See China Manufacturing PMI for April. Bloomberg. 2. China Central Economic Work Conference (CEWC), December 2024. 3. IMF Working Paper, ‘Credit Booms – Is China Different’, Sally Chen and Joong Shik Kang, January 2018, and Autonomous / Columbia Threadneedle Investments’ estimates / CEIC. 4. There are numerous examples: Sweden in the 1980s, Japan in the 1990s, and Spain, Ireland and the US in the 2000s. See also: IMF Working Paper, ‘Systemic Banking Crises Revisited’, Luc Laeven and Fabian Valencia, September 2018. 5. IMF Working Paper: ‘Credit Booms – Is China Different’, Sally Chen and Joong Shik Kang, January 2018, NBER ‘Growth in a time of debt’ Reinhart and Rogoff, 2010, Columbia Threadneedle estimates & Autonomous on China Banks, September 2024. 6. Columbia Threadneedle estimates based on company reports, 2025. 7. Columbia Threadneedle estimates and US Federal Reserve / Bank of Japan / Autonomous data, April 2025. 8. China Banking and Insurance Regulatory Commission, September 24. Covers loans to Commercial Real Estate and small and medium-sized enterprises. 9. Columbia Threadneedle Investments’ analysis of company reports / Emerging Advisors Group / Autonomous, April 2025 10. CICS, China’s Slow-Motion Financial Crisis Is Unfolding as Expected, September 2022. 11. Columbia Threadneedle Investments’ analysis of company reports / Emerging Advisors Group / Autonomous, April 2025. 12. NBER, ‘The aftermath of financial crises’, Carmen M. Reinhart and Kenneth S. Rogoff, 2009. 13. Columbia Threadneedle Investments’ estimates & Autonomous research, April 2025. 14. ECB, The anatomy of a peg: lessons from China’s parallel currencies, by Bahaj and Reis, October 2023 / Emerging Advisors Group / BIS, The size of foreign exchange reserves by Arslan and Cantu, December 2019 15. US Federal Reserve, Abandoning a currency peg by Clement and Polansky, October 2016 / IMF, ‘China stumbles but is unlikely to fall’, E Prasad, December 2023

China small/medium

Europe

US

China

5

7

9

11

13

15

“Allowing the LDI manager discretion to trade on a scheme’s behalf, as would be the case when combining investment grade credit with the LDI manager, significantly streamlines the transaction process”

For pension scheme trustees, an integrated solution for LDI and investment-grade credit offers benefits, particularly from an investment and governance standpoint.

We shine a light on often under-discussed but important factors to think about when structuring your LDI portfolio framework. Here we unpick the benefits of an integrated solution of holding investment grade credit with the LDI manager. Historically, pension schemes have had different portfolios for different purposes, which were often run by different managers. Consolidation starts to happen when schemes get closer to their endgame, but we would argue there is also great benefit in reducing the governance burden when the investment strategy is more complex. This is especially true for the fixed income part of the portfolio. The reason why pension schemes hold investment grade credit in their portfolios is to: a) complement the hedging obtained from the LDI portfolio; b) act as collateral support; c) provide an additional return above gilts; and d) generate cashflows for benefit payments. The level of crossover with the LDI portfolio is significant, so separating the credit from the LDI portfolio is suboptimal.

Adil Gulamali Client Director, UK Institutional

While there is some nuance between pooled and bespoke solutions, in both instances a full toolkit helps the LDI manager create a better hedge profile by incorporating credit into the solution. In a fully bespoke LDI and credit portfolio, there is also more freedom for the investment manager to optimise the scheme’s credit holdings as the LDI toolkit can be used to smooth cashflows.

Hedge profile